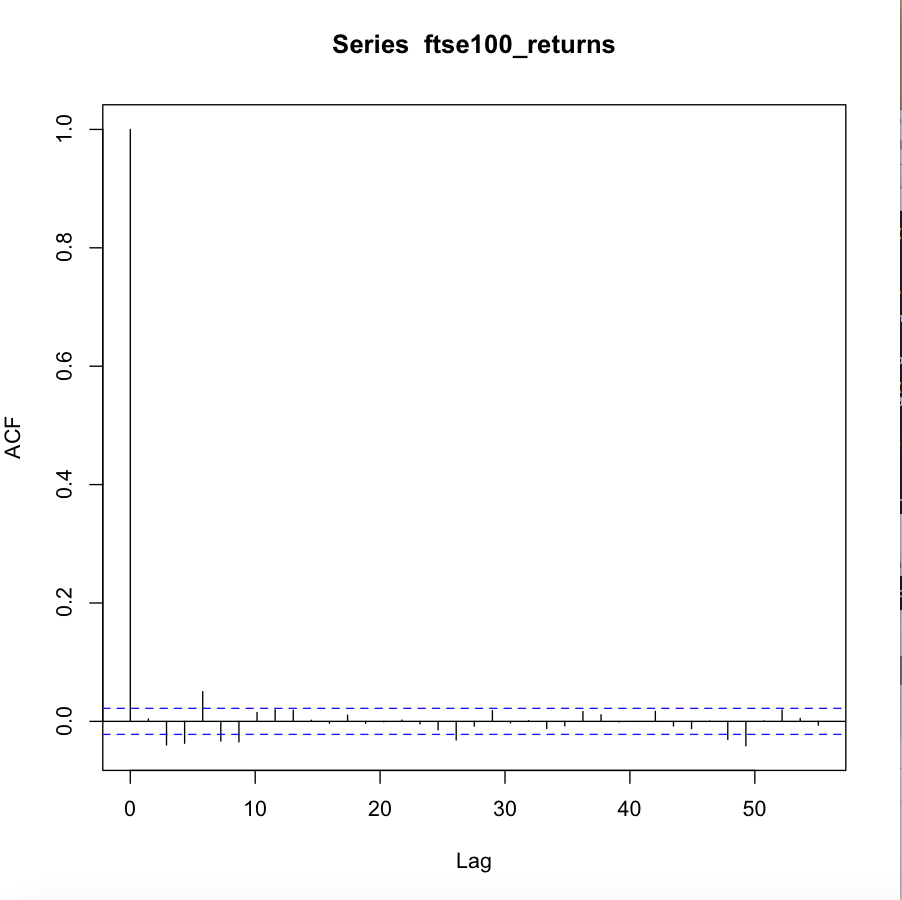

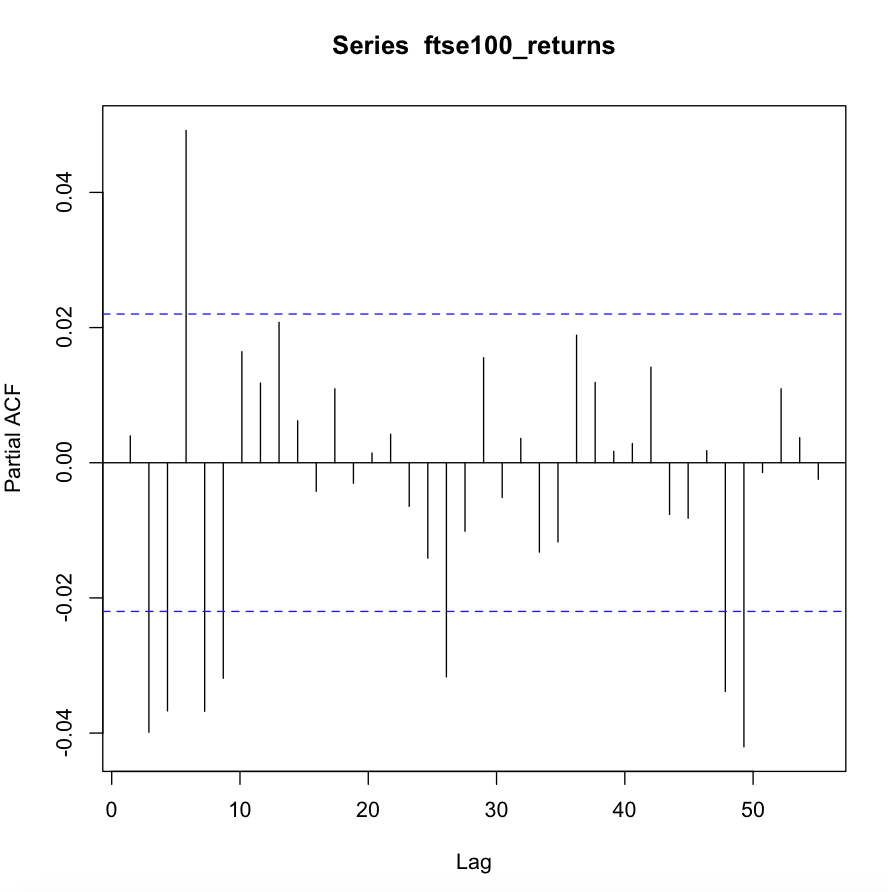

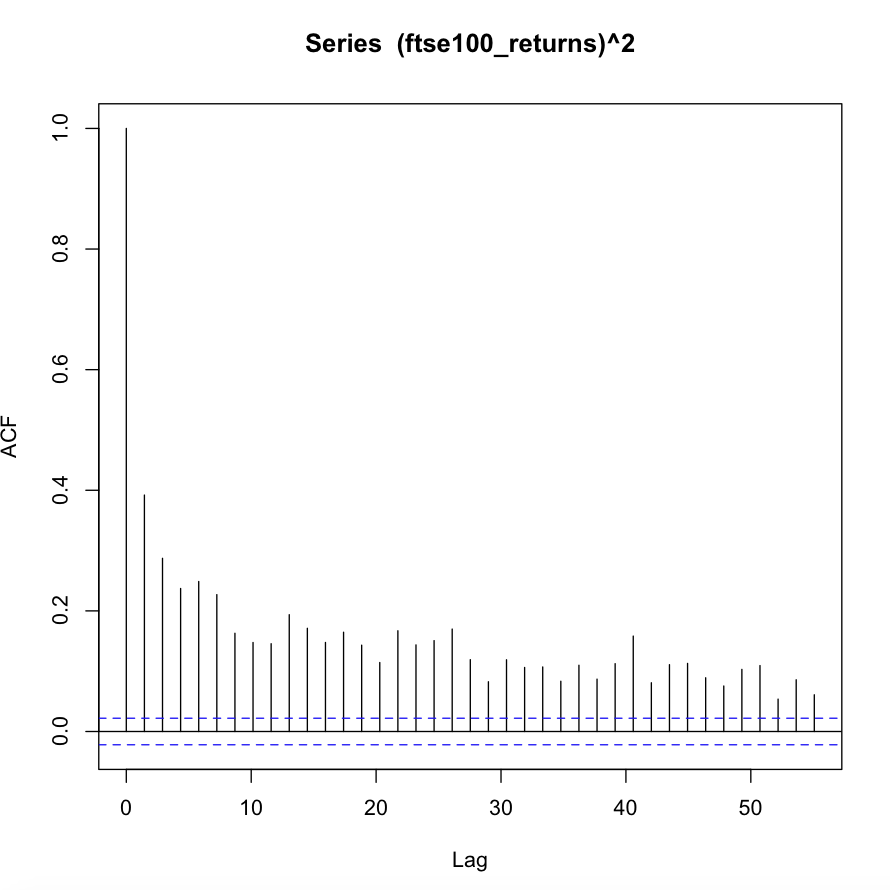

I'm trying to fit an ARMA-GARCH model to a data set of FTSE 100 log returns (which I've uploaded here). However, I'm not able to find a well-fitting model. Below are the ACF and PACF of the log return series and the ACF of the squared log return series. Looking at the ACF of the squared series, there seems to be conditional heteroscedasticity present in the data, making an ARCH or GARCH model appropriate. At the same time there seem to be significant autocorrelations, making an ARMA-type model for the conditional mean appropriate.

Fitting ARMA(p,q)-GARCH(1,1) models of various orders (p,q) and selecting by AIC, I choose p = 1, q =2. However, the model doesn't seem to provide a decent fit as indicated by the following output:

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 3.847 0.04983

Lag[2*(p+q)+(p+q)-1][8] 5.474 0.06272

Lag[4*(p+q)+(p+q)-1][14] 10.146 0.10862

d.o.f=3

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 11.11 0.0008589

Lag[2*(p+q)+(p+q)-1][5] 12.32 0.0022979

Lag[4*(p+q)+(p+q)-1][9] 12.75 0.0121929

d.o.f=2

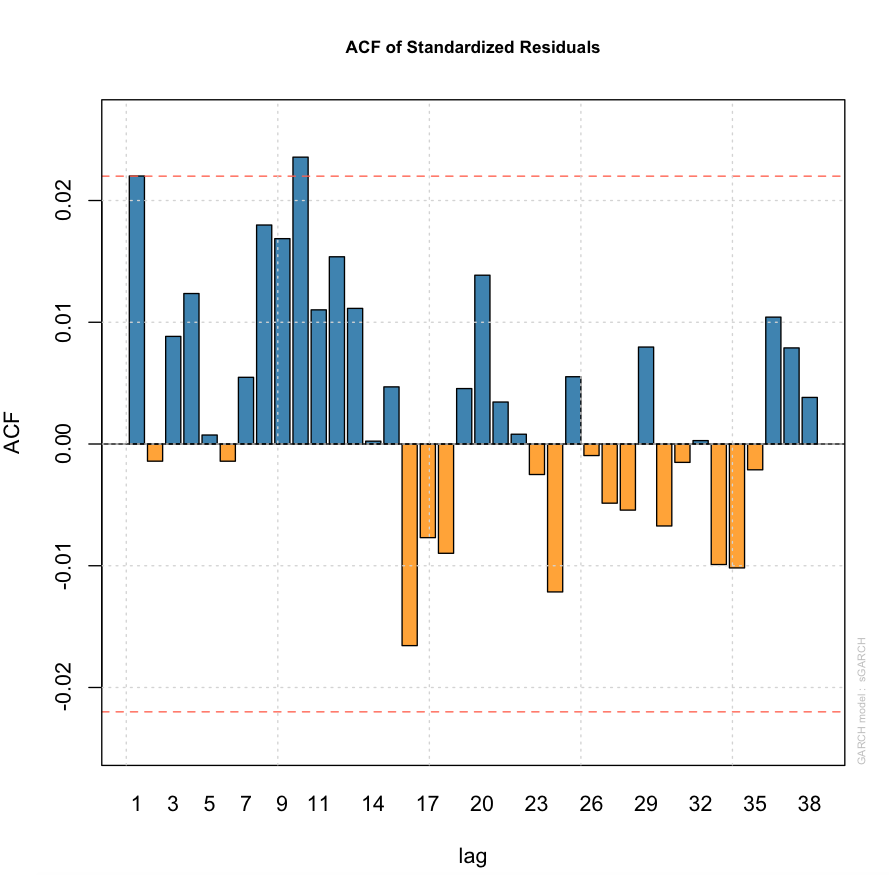

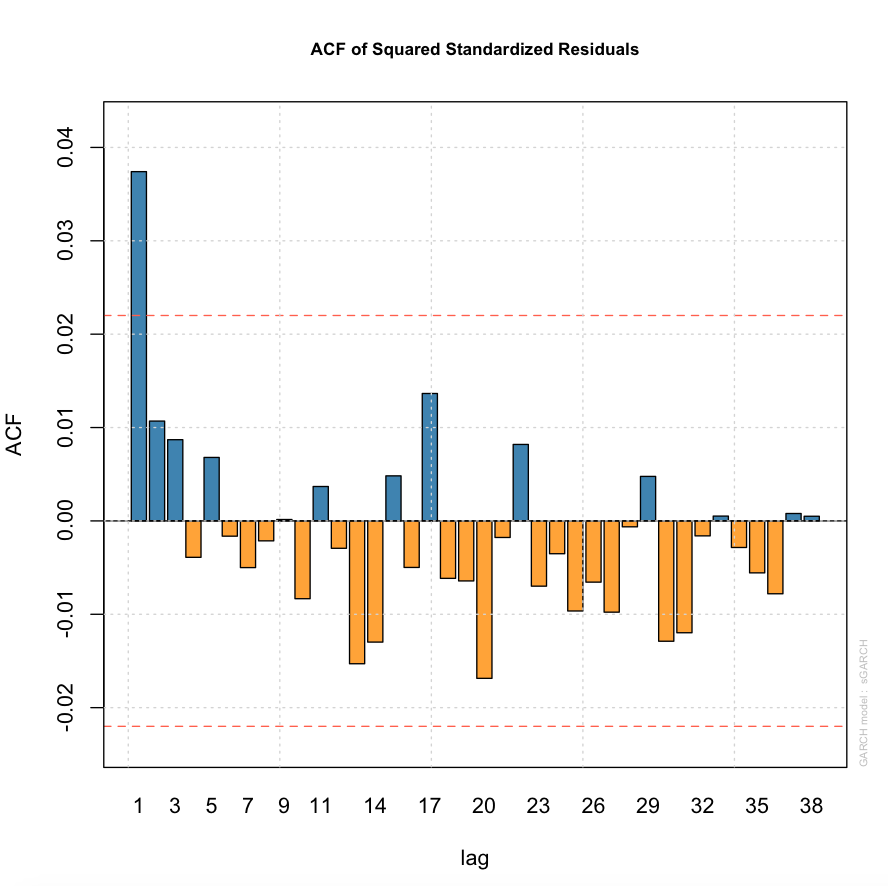

On the other hand, the ACF of the standardised residuals and the squared standardised residuals look okay (see below). My question is whether my model selection mechanism (AIC is in this case) is appropriate for the data set at hand (despite the hypothesis test results given above).