it's a first time I am running regressions for my dissertation and really need your help. I haven't been studying econometrics before, so I don't know if what I am doing is right or wrong.

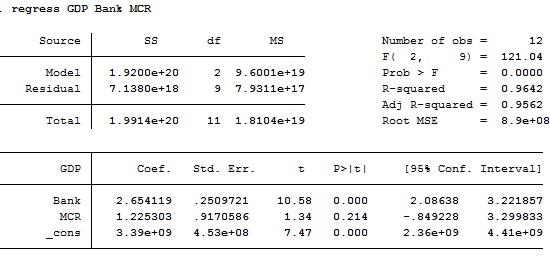

I am looking at the relative effect of banking sector and capital markets on the economy of a particular country, so I wonder how can I interpret this result:

In the model "Bank" is average annual value of deposits at banks deflated by respective inflation rate and "MCR" is real market capitalisation

I am concerned with the very high value of R2 and a high p value of MCR. Can I conclude based on the model that the effect of banks is significant and in terms of markets, they are not yet developed to the stage that will positively impact the economic growth.

Looking forward to your replies!