This is really puzzling...

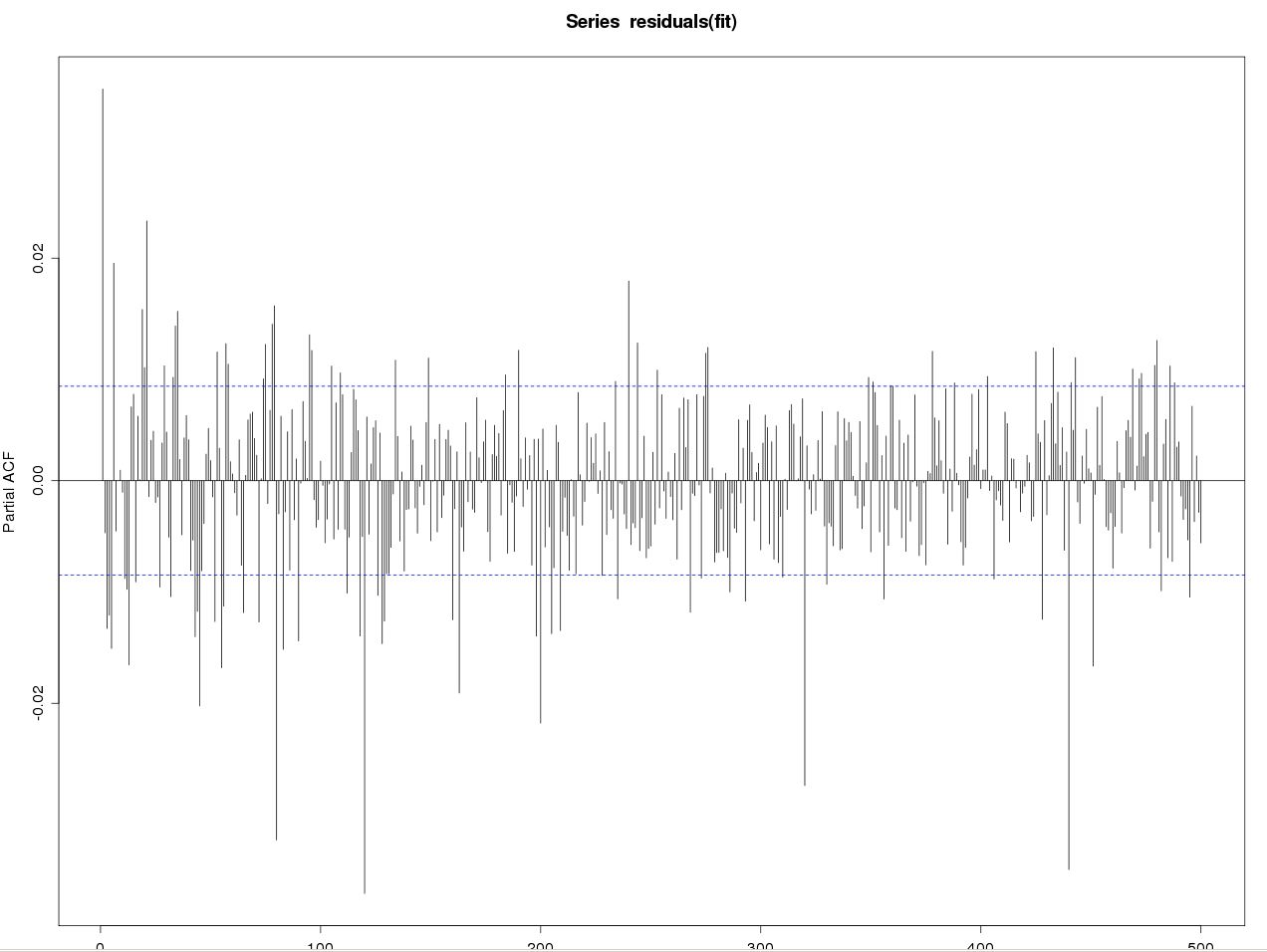

I have this data which has a lot autocorrelations...

The data is about 60000 data points of 15min data.

I tried fitting it to ARIMA(6, 0, 6) and even GARCH(1, 1) with mean model ARMA(6, 6), still there are lots of autocorrelations in the residuals.

I almost wanted to try ARIMA(100,0,100), but I think even that is not enough...

I almost wanted to try ARIMA(100,0,100), but I think even that is not enough...

I am doing these in R.

How to I get out this swamp? Please shed some lights on me.

Thanks so much

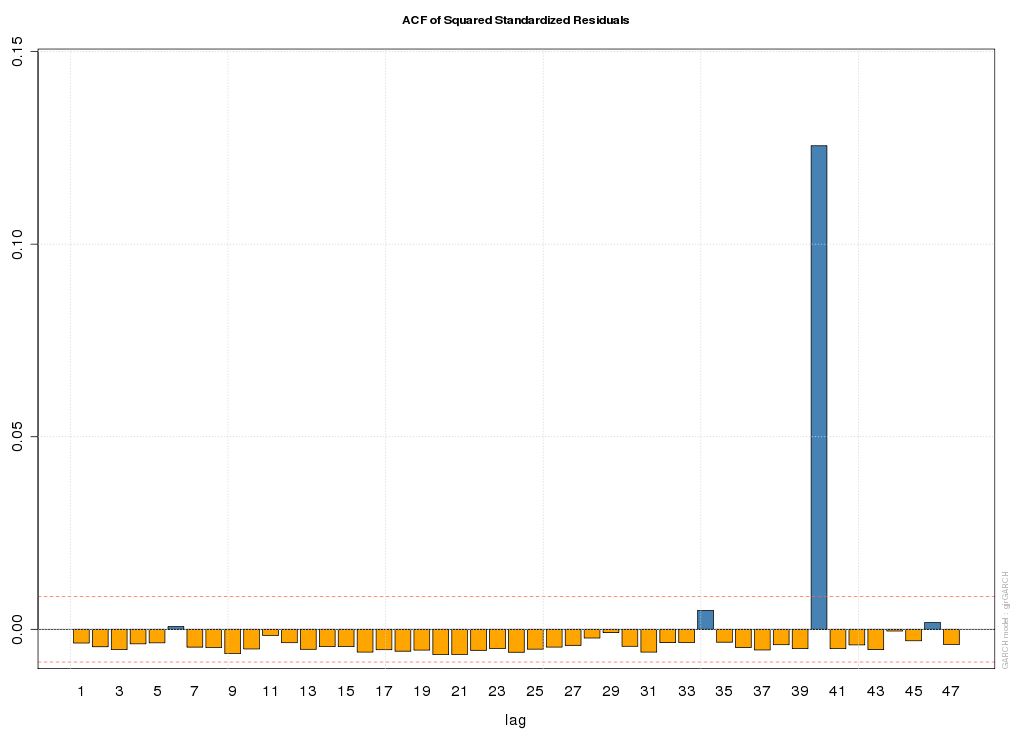

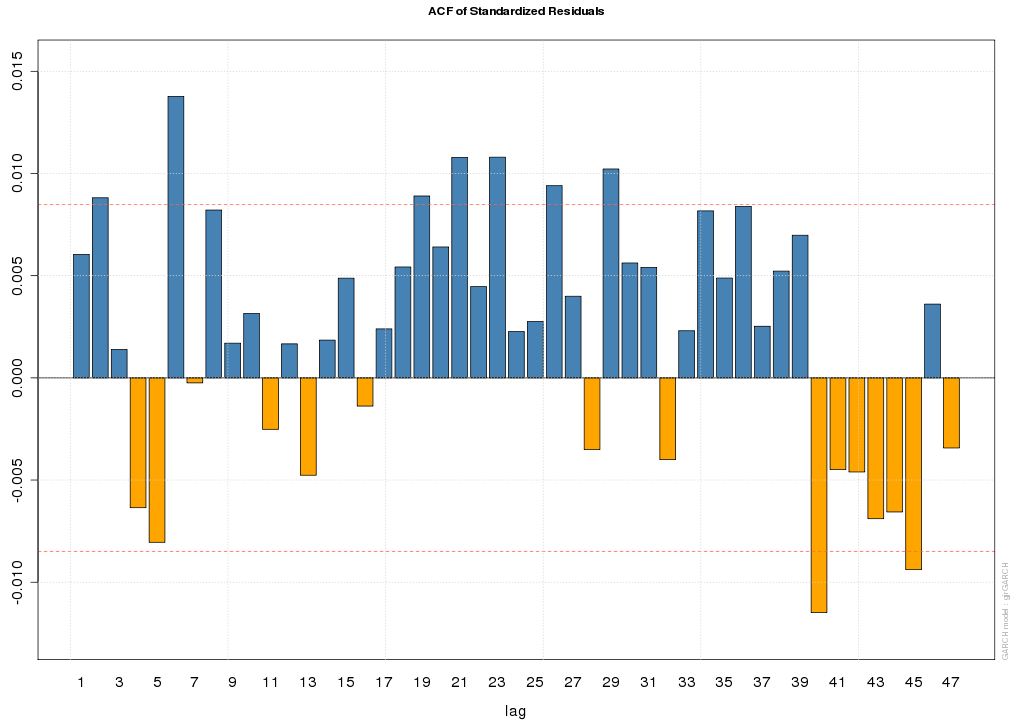

Update: I have fitted a gjrGARCH model with distribution "sstd" in R using "rugarch" package...

QQ-Plot of Standardized Residuals looks great - it's a straight line...

However the ACF plots of the residuals and the residuals squared are a bit strange, especially the big spike in the residual squared ACF plot.

Could anybody please shed some lights on us, esp about that big spike?

Thank you!