I need to make a composite index from the sum of three power-law distributed variables, which vary on different scales and have different variances. For each variable there are many observations with very low scores and few observations with high scores.

I need to normalize the variables to obtain a common scale, before summing them to obtain a single score of the final index. I'm considering two possibilities:

Min-Max Normalization

(Xi - min (X)) / (max(X) - min(X))

Standardization (Z-scores)

(Xi - mean(X)) / std(X)

Which solution is appropriate, given the power-law distribution of the three variables? Or are they both wrong? Why?

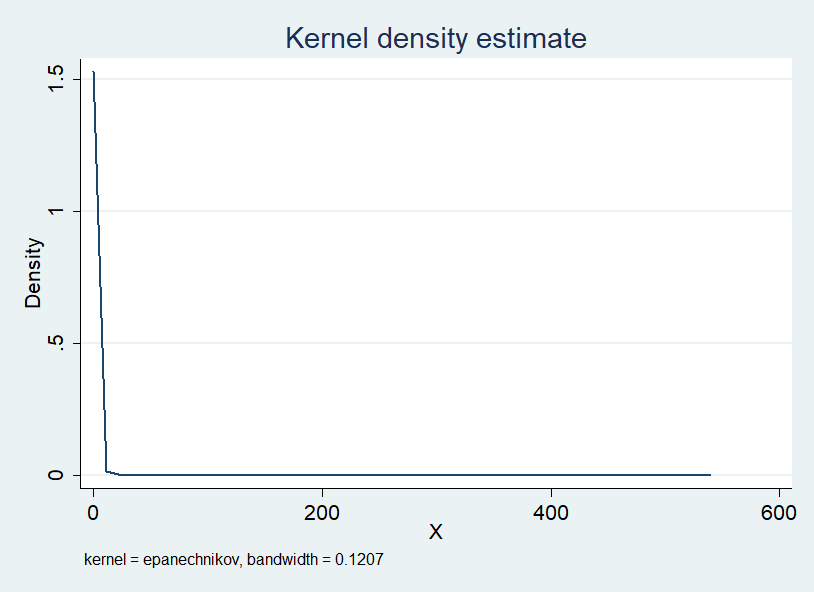

EDIT Please have a look to an example of the distribution I am referring to:

I have three variables distributed like X and I need to normalized them before making a sum of the three.