I use auto_arima from python library pmdarima.arima to predict a time series. However, the model seems not work on my data because the prediction results of both training and test data are pretty bad. I would like to know it is because somewhere I did wrong or the data is unpredictable by ARIMA. Here is what I did.

b is my 5-month time series with 700 observations evenly distributed. I first checked if the data is stationary by ADCF.

from statsmodels.tsa.stattools import adfuller

print("Results of Dicky-Fuller Test:")

dftest = adfuller(b, autolag='AIC')

dfoutput = pd.Series(dftest[0:4], index=['ADF Statistic','p-value','#Lags Used','Number of Observations Used'])

for key,value in dftest[4].items():

dfoutput['Critical Value (%s)'%key] = value

print(dfoutput)

The results are here

-----------------------------------------

Results of Dicky-Fuller Test:

ADF Statistic -2.045778

p-value 0.266868

#Lags Used 9.000000

Number of Observations Used 690.000000

Critical Value (1%) -3.439863

Critical Value (5%) -2.865738

Critical Value (10%) -2.569005

dtype: float64

-----------------------------------------

It looks a stationary data to me. Then I use auto_arima to find the best parameter combinations and do the fit as well as prediction

from pmdarima.arima import auto_arima

model = auto_arima(b, start_p=1, start_q=1,

max_p=6, max_q=6, m=1,

seasonal=False,

d=0, trace=True,

error_action='warn',

suppress_warnings=True,

stepwise=True)

print(model.aic())

model.fit(train)

prediction1 = model.predict(n_periods=len(train))

prediction2 = model.predict(n_periods=len(test))

#plot the predictions for validation set

plt.plot(time_train,train, label='train')

plt.plot(time_test,test, label='test')

plt.plot(time_train, prediction1, label='prediction1')

plt.plot(time_test, prediction2, label='prediction2')

plt.legend()

plt.show()

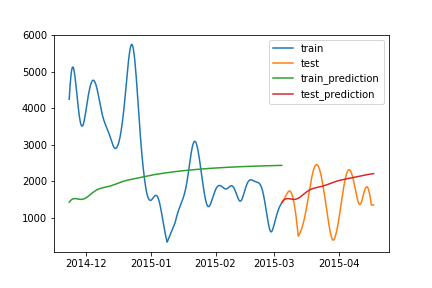

And the results are

Could anyone please tell me what I did wrong? Thanks! Edit: I understand that the train_prediction curve shown above is actually not the prediction of training data -- it is the predictions of time series len(train) time stamps after the traning data.