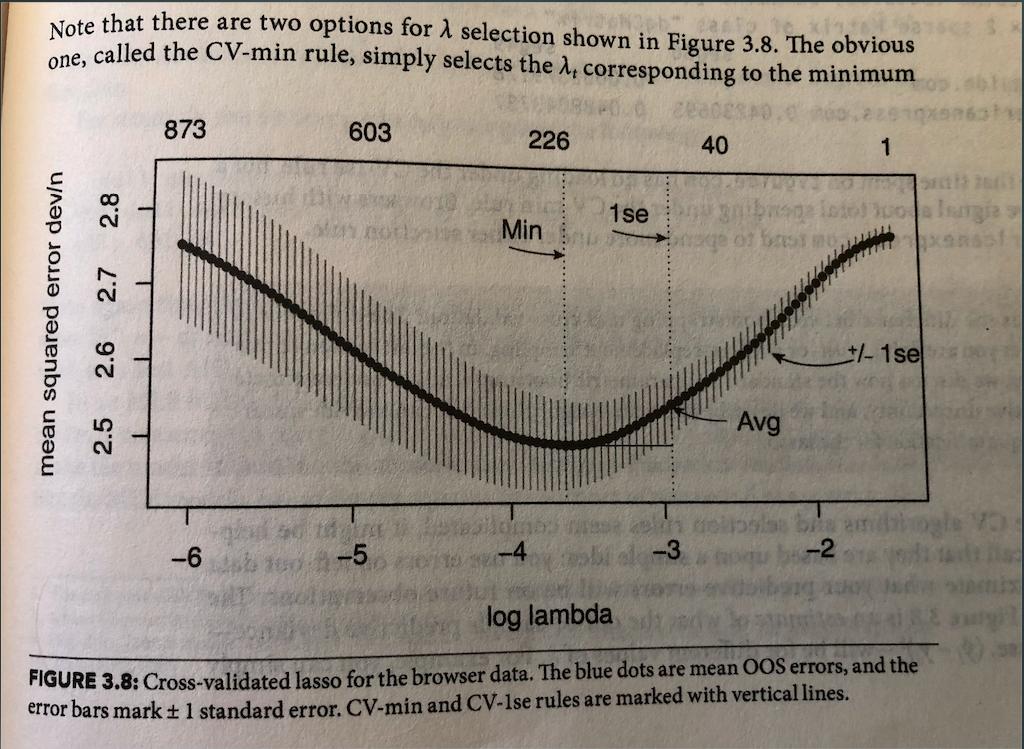

I'm hoping to reproduce the following figure from Matt Taddy's book Business Data Science using the Happiness data set from Kaggle.

Running linear regression using lasso regularization, he observes a minimum in the out-of-sample (OOS) mean squared error and asserts that this value of lambda represents a good choice for regularization. Makes sense.

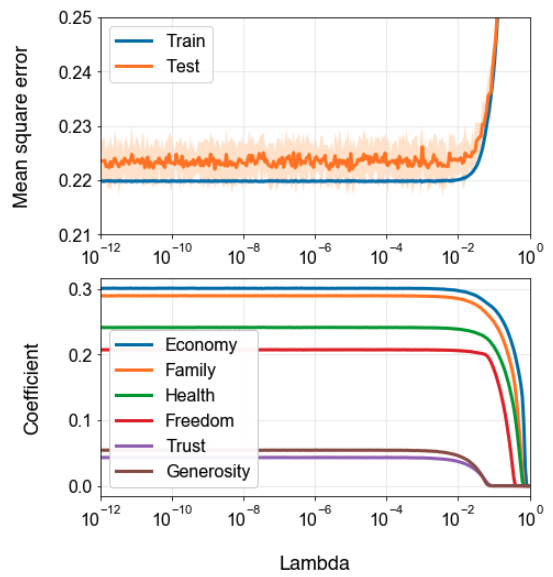

When I try the same thing on the happiness data set, a couple things look right: in-sample MSE is lower than out-of-sample MSE, and coefficients go to zero as regularization parameter is increased.

However, I don't see any drop in out-of-sample mean squared error with increasing lambda -- it's noisy and flat (top plot, orange trace).

As I understand it, dialing up lambda (sklearn.linear_model.Lasso() calls this alpha) should reduce OOS MSE as the fitted coefficients generalize better to the unseen data.

Why might I not be seeing a minimum in OOS MSE?

I wrote up the code myself because I wanted to understand how it works. I used 10-fold cross-validation with shuffled sampling and scanned 300 points across the regularization range of 10^-12 <= alpha <= 1.

Here it is:

# k-fold cross validation with lasso regularization

import numpy as np

alphas = np.logspace(-12, 0, 301)

coefs_all = []

coefs_avg_all = []

coefs_std_all = []

mse_train_avg_all = []

mse_test_avg_all = []

mse_train_std_all = []

mse_test_std_all = []

for alpha in alphas:

# randomly split data into k folds

from sklearn.model_selection import KFold

folds = 10

kf = KFold(n_splits=folds, shuffle=True)

coefs = []

mse_train = []

mse_test = []

for train_index, test_index in kf.split(X):

X_train, X_test = X.iloc[train_index], X.iloc[test_index]

y_train, y_test = y.iloc[train_index], y.iloc[test_index]

# build model on training data and get coefficients

from sklearn import linear_model

lasso = linear_model.Lasso(alpha=alpha)

lasso.fit(X_train, y_train)

coefs_fold = lasso.coef_

# get mean squared error of model predictions

y_pred_train_fold = np.dot(X_train, coefs_fold)

y_pred_test_fold = np.dot(X_test, coefs_fold)

mse_train_fold = sum((y_train - y_pred_train_fold) ** 2) / len(y_train)

mse_test_fold = sum((y_test - y_pred_test_fold) ** 2) / len(y_test)

# for each fold, add coeffs and mses to growing list

coefs.append(coefs_fold)

mse_train.append(mse_train_fold)

mse_test.append(mse_test_fold)

# across folds at this alpha, get average values of coefficients, mses, and stdevs

coefs_avg_alpha = [sum(items) / len(coefs) for items in zip(*coefs)]

coefs_std_alpha = [np.std(items) for items in zip(*coefs)]

mse_train_avg_alpha = np.average(mse_train)

mse_test_avg_alpha = np.average(mse_test)

mse_train_std_alpha = np.std(mse_train)

mse_test_std_alpha = np.std(mse_test)

# compile these average values into growing list

coefs_avg_all.append(coefs_avg_alpha)

coefs_std_all.append(coefs_std_alpha)

mse_train_avg_all.append(mse_train_avg_alpha)

mse_test_avg_all.append(mse_test_avg_alpha)

mse_train_std_all.append(mse_train_std_alpha)

mse_test_std_all.append(mse_test_std_alpha)

# compile mean square error summary into dataframe

mse_df = pd.DataFrame({'Alpha': alphas,

'MSE train avg': mse_train_avg_all,

'MSE test avg': mse_test_avg_all,

'MSE train std': mse_train_std_all,

'MSE test std': mse_test_std_all})

# bind coefficients to previous dataframe

coefs_df = pd.DataFrame(coefs_avg_all, columns=X.columns.to_list())

lasso_cv_summary_df = pd.concat([mse_df, coefs_df], axis=1)

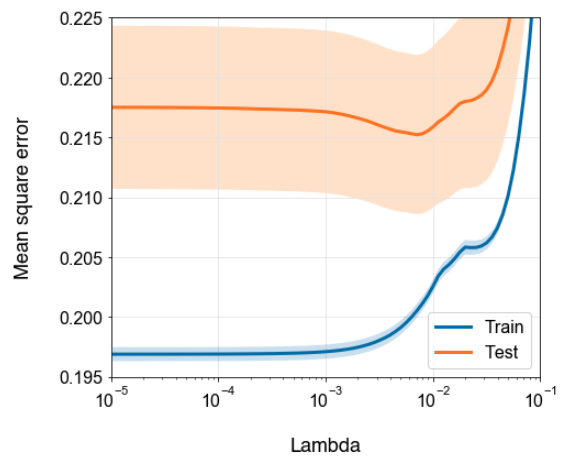

sklearn.preprocessing.StandardScaler. This is really important, since you want all your features to have the same scale properties so that the regularization penalty applies fairly across all of them. $\endgroup$StandardScalerby subtracting the mean and dividing by the standard deviation (df_norm = ( df - df.mean() ) / df.std()). I will take your advice and invert the order of alpha and CV loops to see how OOS MSE vs. alpha looks with the same train and test sets across alpha. $\endgroup$shuffle=FalseinKFold()accomplishes the same thing. However, OOS MSE vs. alpha remains perfectly flat! At no value of alpha does the model perform better on unseen data than the unregularized (i.e., alpha=0) model. This is surprising to me and I'm still thinking that something's probably not right with my code. $\endgroup$