Hi i am fitting a Lasso model using different values in the range of 2*10^-5 to 500 for the alpha parameters like:

alphas=np.linspace(0.00002,500,20)

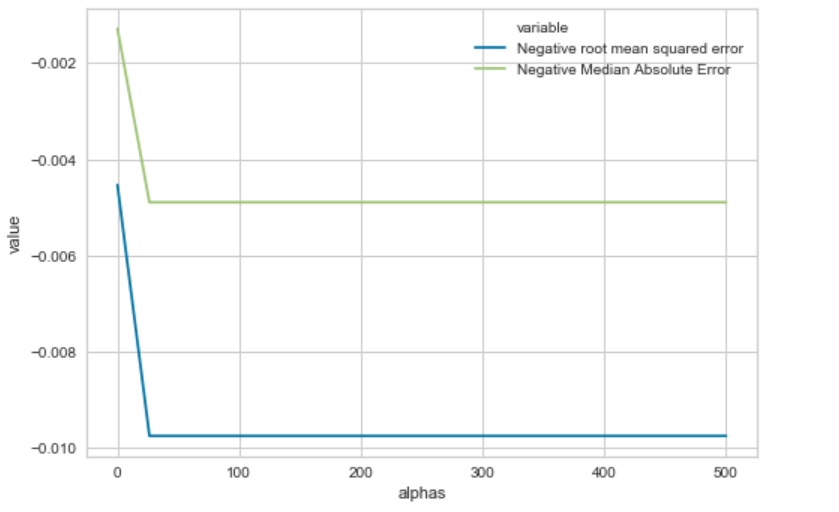

when i plot the negative root mean squared error and absolute error from cross validation i get a graph like this:

so the error increases in modulo instead of decreasing... why am i getting this result?