I was approaching Cox regression and need to evaluate whether is more suitable to model my independent variable as a non-linear prediction of the outcome.

Main questions is:

- How do I check whether or not my independent variable should be modelled in a non-linear fashion?

I came into several methods, one of which was to plot the variable versus the martingale-based residual of the Cox regression (See for example www.sthda.com/english/wiki/cox-model-assumptions, last figures).

I therefore produce this type of plot with the following code, being var my independent variable:

time <- data$time

status <- data$status

S <- Surv(time, status)

model1 <- coxph(S~1, data = data)

data$residual <- residuals(model1, type = "martingale")

ggplot(data = data, mapping = aes(x = var, y = residual)) +

geom_point() +

geom_smooth()

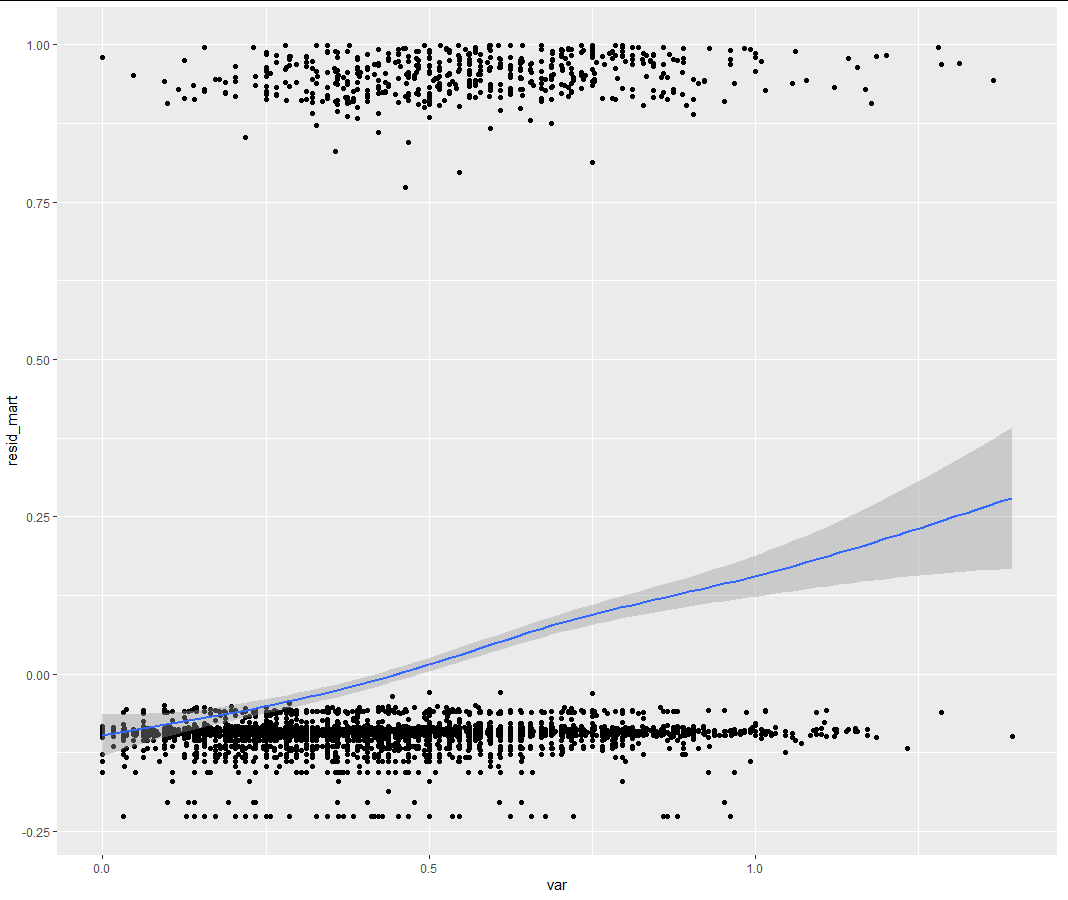

Here is the result:

Here comes the other questions:

- As you can see, in my plot martingale-based residuals seems to be a lot "clustered" at extreme values, different from other plots that I found online in which residuals were more or less "uniform". I don't know how to interpret this data - seems like the data are "splitted".

- Based on the plot, should I assume a linear relationship? I was considering to use a restricted cubic spline with 4 knots, since my guess was that a non-linear relationship may be the case here.

- What is the correct interpretation of this plot? Do anyone have a guidance paper to interpret this plots and/or more generally speaking a guide to Cox diagnostics?

[EDIT]

This is the result of the model and of the anova as requested by @EdM - actually to generate this result I have fitted model2 with cph.

Model:

Coef S.E. Wald Z Pr(>|Z|)

var 4.5077 1.5089 2.99 0.0028

var' -0.1702 4.8386 -0.04 0.9719

var'' -5.4636 12.5472 -0.44 0.6632

Anova:

Wald Statistics Response: S

Factor Chi-Square d.f. P

var 217.03 3 <.0001

Nonlinear 17.17 2 2e-04

TOTAL 217.03 3 <.0001