Given $X_1, X_2,..., X_n $ i.i.d. random variables.

$E[X_i] = \mu_1 \in \mathbb{R} $ $\&$ $ V[X_i] = \sigma_1^2 \in \mathbb{R}^+$ $\forall i \in \{1,2,3,...,n\}$.

The statistics $\bar{X} = \frac{X_1 + X_2 + ... + X_n}{n}$ converges in distribution to $Z_1 \sim N(\mu_1, \frac{\sigma_1^2}{n}$) according to the Central Limit Theorem.

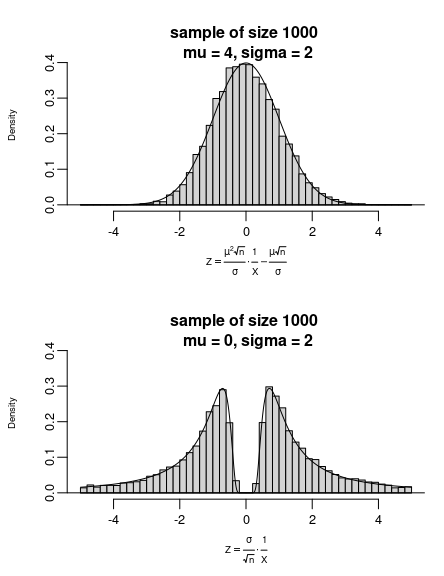

Does $\frac{1}{\bar{X}}$ converge in distribution to $\frac{1}{Z_1}$?

I guess the answer is NO, but I decided to ask the question here for more insights. A simple yes/no answer without any explanation would be appreciated too.

The reason I ask this question is relevant to ratio estimator in survey sampling as I read in some books that we could assume the ratio estimator $\hat{R} = \frac{\bar{X}}{\bar{Y}}$ to be normally distributed.

If I am not mistaken, if $X_n$ converges in distribution to $X$, and $Y_n$ converges in distribution to $Y$, then $X_nY_n$ converges in distribution to $XY$

Given $Y_1, Y_2,..., Y_n $ i.i.d. random variables.

$E[Y_i] = \mu_2 \in \mathbb{R} $ $\&$ $ V[Y_i] = \sigma_2^2 \in \mathbb{R}^+$ $\forall i \in \{1,2,3,...,n\}$.

The statistics $\bar{Y}$ converges in distribution to $Z_2 \sim N(\mu_2, \frac{\sigma_2^2}{n}$) according to the Central Limit Theorem.

If $\frac{1}{\bar{Y}}$ converges in distribution to $\frac{1}{Z_2}$, $\frac{\bar{X}}{\bar{Y}}$ converges in distribution to $\frac{Z_1}{Z_2}$, which is a fat-tailed "Cauchy" distribution with not well-defined expected value and variance.

Therefore, it is incorrect to assume that the ratio estimator $\hat{R} = \frac{\bar{X}}{\bar{Y}}$ is normally distributed.