For my Master thesis I have to perform the DCC-GARCH model to examine the correlation between real estate house prices and the stock market. I tested the data for normality (both not normal) and stationarity (both not stationary) and variance ratio test (was significant).

I used the log function because of the non-normality and took the first difference. After this, the real estate house prices were still not stationary, so I took the second difference which resulted in stationary data. The stock market data was stationary after taking the first difference, but I think I need to take the second difference as well in order to use it for the DCC-GARCH model.

The code I used for the DCC model is:

#perform DCC

model1=ugarchspec(mean.model = list(armaOrder=c(0,0)),variance.model = list(garchOrder=c(1,1),model="sGARCH"),distribution.model = "norm")

modelspec=dccspec(uspec = multispec(replicate(2,model1)),dccOrder = c(1,1), distribution = "mvnorm")

modelfit=dccfit(modelspec,data=(data.frame(ts_nominal,ts_share)))

modelfit

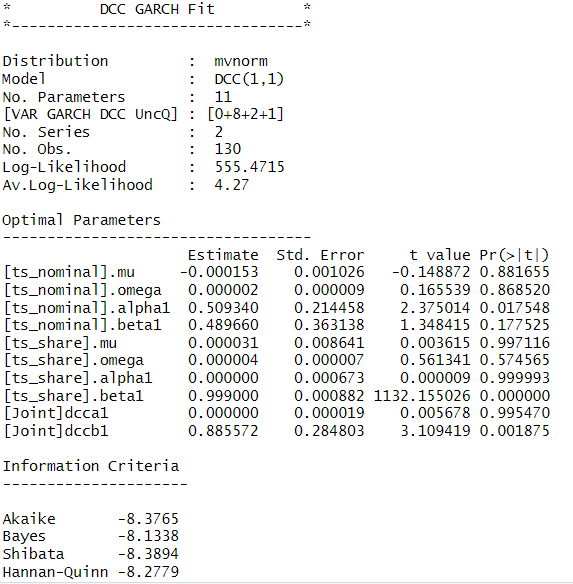

I'm not sure if I took the right steps to perform this analysis or if my code is even correct. Compared to other papers, I find it strange that only 3 parameters are significant and that alpha1 for stocks and dcca1 are almost equal to 1.

Can anyone help me with this?

Update: Further Research

I have proceeded by taking the log return of both the property price index and stock price index. Then I used the diff() function, resulting in both time series being stationary. The results, however, are barely different than the last results I showed in the post.

Distribution : mvnorm

Model : DCC(1,1)

No. Parameters : 11

[VAR GARCH DCC UncQ] : [0+8+2+1]

No. Series : 2

No. Obs. : 130

Log-Likelihood : 502.7599

Av.Log-Likelihood : 3.87

Optimal Parameters

-----------------------------------

Estimate Std. Error t value Pr(>|t|)

[ts_prop].mu 0.000547 0.003082 0.177488 0.859125

[ts_prop].omega 0.000011 0.000072 0.156417 0.875704

[ts_prop].alpha1 0.349696 0.649448 0.538451 0.590266

[ts_prop].beta1 0.649304 0.387195 1.676944 0.093553

[ts_share].mu 0.000031 0.008641 0.003615 0.997116

[ts_share].omega 0.000004 0.000007 0.561343 0.574564

[ts_share].alpha1 0.000000 0.000673 0.000009 0.999993

[ts_share].beta1 0.999000 0.000882 1132.157095 0.000000

[Joint]dcca1 0.000000 0.000007 0.000353 0.999719

[Joint]dccb1 0.895265 0.119982 7.461638 0.000000

Information Criteria

---------------------

Akaike -7.5655

Bayes -7.3229

Shibata -7.5784

Hannan-Quinn -7.4669

Elapsed time : 0.909425

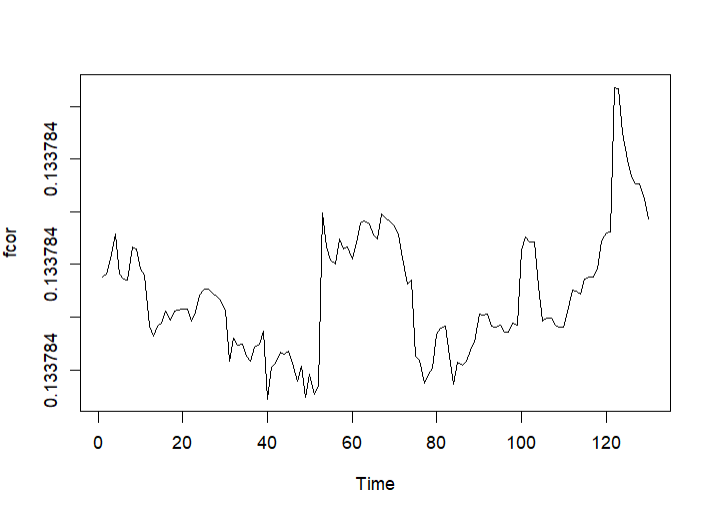

The next step in our analysis is to apply linear regression to see which determinants (like the long term interest rate) have a significant effect on the dynamic correlation between the property return time series and stock return time series. For this, I extracted the dynamic correlations from the DCC-GARCH model, but as you can see in the graph 'fcor', these correlations all have the same value of 0.133784 with minimal changes.

mod1=lm(fcor~long)

> summary(mod1)

Call:

lm(formula = fcor ~ long)

Residuals:

Min 1Q Median 3Q Max

-0.000000010205 -0.000000003962 -0.000000001022 0.000000004495 0.000000019842

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.1337839573855 0.0000000005038 265555616.311 < 0.0000000000000002 ***

long 0.0000000045540 0.0000000016445 2.769 0.00646 **

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.000000005664 on 128 degrees of freedom

Multiple R-squared: 0.05652, Adjusted R-squared: 0.04915

F-statistic: 7.669 on 1 and 128 DF, p-value: 0.006455

I also performed regression on other determinants with all having a significant effect on the dynamic correlations. Can someone explain to me why the dynamic correlations barely change and why this has an effect on the linear regression result?

diff(log(...))with a single difference)? Also, what do you mean by variance test? Also, next time consider pasting the R output as text, not as picture. $\endgroup$diff(log(.))appears nonstationary, but it does not seem to have a unit root, and thus taking another difference is probably not an adequate measure. In this model, I would perhaps just use thediff(log(.))as is, even if it is nonstationary. But I do not have a solid defense of either choice. The problem is that the model is inadequate in either case due to the first series exhibiting some form of structural change. $\endgroup$