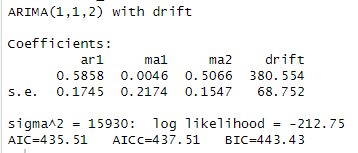

I obtained the following output from the function auto.arima():

Is this the correct way to write the equation?

Or should it be like this?

I obtained the following output from the function auto.arima():

Is this the correct way to write the equation?

Or should it be like this?

Hi: you don't difference the error terms. So, the arima(1,1,2) is:

$ y_{t} - y_{t-1} = \mu + \phi (y_{t-1}-y_{t-2}) + \theta_{1} \epsilon_{t-2} + \theta_2 \epsilon_{t-1} + \epsilon_t$.

So, the left side is for the $d=1$ term. The first term is the mean ( what you refer to as drift ? ), the second term is the $p= 1$ term and the third and fourth terms are the $q=2$ MA terms.

Sometimes there is the possibility the $\mu$ is put as part of the $\phi$ term rather than alone but I'd have to look at the code for auto.arima in R and don't have time at the moment. I hope this helps.