Equality-null hypothesis tests are entirely the wrong tool for model selection.

People only tend to notice when sample sizes are very large. However, they usually draw the wrong conclusion in that instance; rather than realizing that the test they used doesn't answer the question they needed an answer to, they decide that hypothesis tests are broken.

Pushing up p-values by sub-sampling the data is a commonly used strategy in response to the problem, but it's quite misguided — arbitrarily throwing out information doesn't solve the problem, it merely disguises the issue, leaving the underlying problem (that it's the wrong tool for the job in any case) untouched.

The reason why the p-values are small is not just that the sample size is large — it's that no simple form distributional model is correct. Correctness is not even the purpose of models.

In short, to quote George Box "Remember that all models are wrong; the practical question is how wrong do they have to be to not be useful". Models should be chosen - when they must be chosen at all - with regard to their purpose.

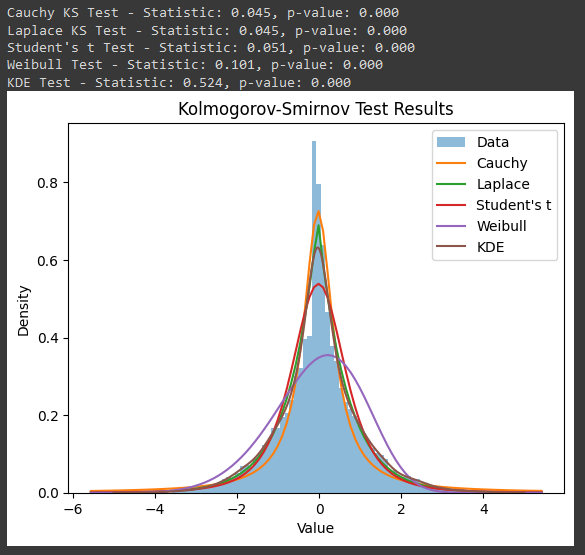

You say you need "to define a distribution for the sample so that I can plot all possible outcomes" but the approach you have used doesn't solve that problem. You're choosing between models that define the distribution outside the range of the data, sure, but there's no guarantee whatever that the process follows any of your arbitrarily-selected laundry list of distributions where you don't have data, and no obvious reason to imagine they should.

If the empirical distribution of the data themselves will not serve because you want a distribution where you don't have data, then your problem is that you demand information where you have none. Selection from the arbitrary laundry list of distributions you happen to choose to select between does not solve that problem either — again, it just disguises it. In short, that, too, is using the wrong tool for the task.

If you really want to know about the distribution where there are no data you have to bring in some external information, whether from theory, consideration of the processes involved, other data, etc. It requires more effort than presuming that fit over here implies fit way over there, but it has a somewhat better hope of avoiding potentially very misleading answers.