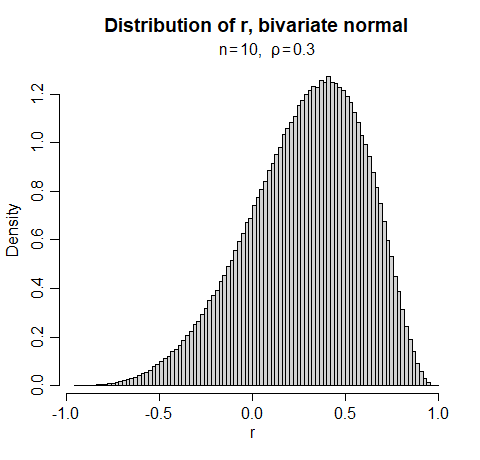

I have an $x$ and a $y$ that I would like to find the correlation of to learn more about their relationship. Unfortunately, I only have $10$ points. Can I in good faith use the Pearson correlation coefficient (are there generally accepted rules for when to not use it in the case of dataset size)? Is there some sort of alternative correlation that is recommended for a situation like this?

If it's relevant, I actually have lots of $x$s and $y$s with $10$ points each, and I'm using the correlation coefficient to summarize what I see. Visual inspection by graph shows a lot of mixed results (a couple look somewhat linear and give a Pearson correlation coefficient around $0.8$, but most have odd non-linear relationships).