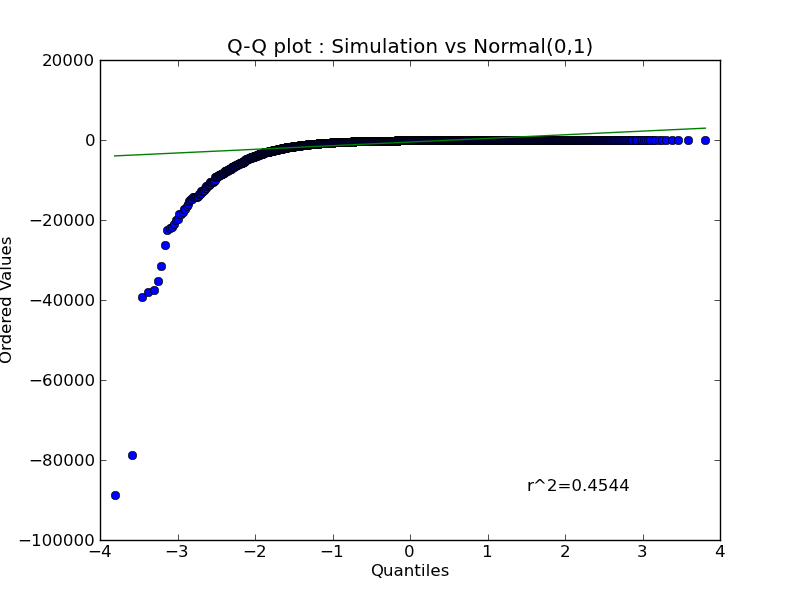

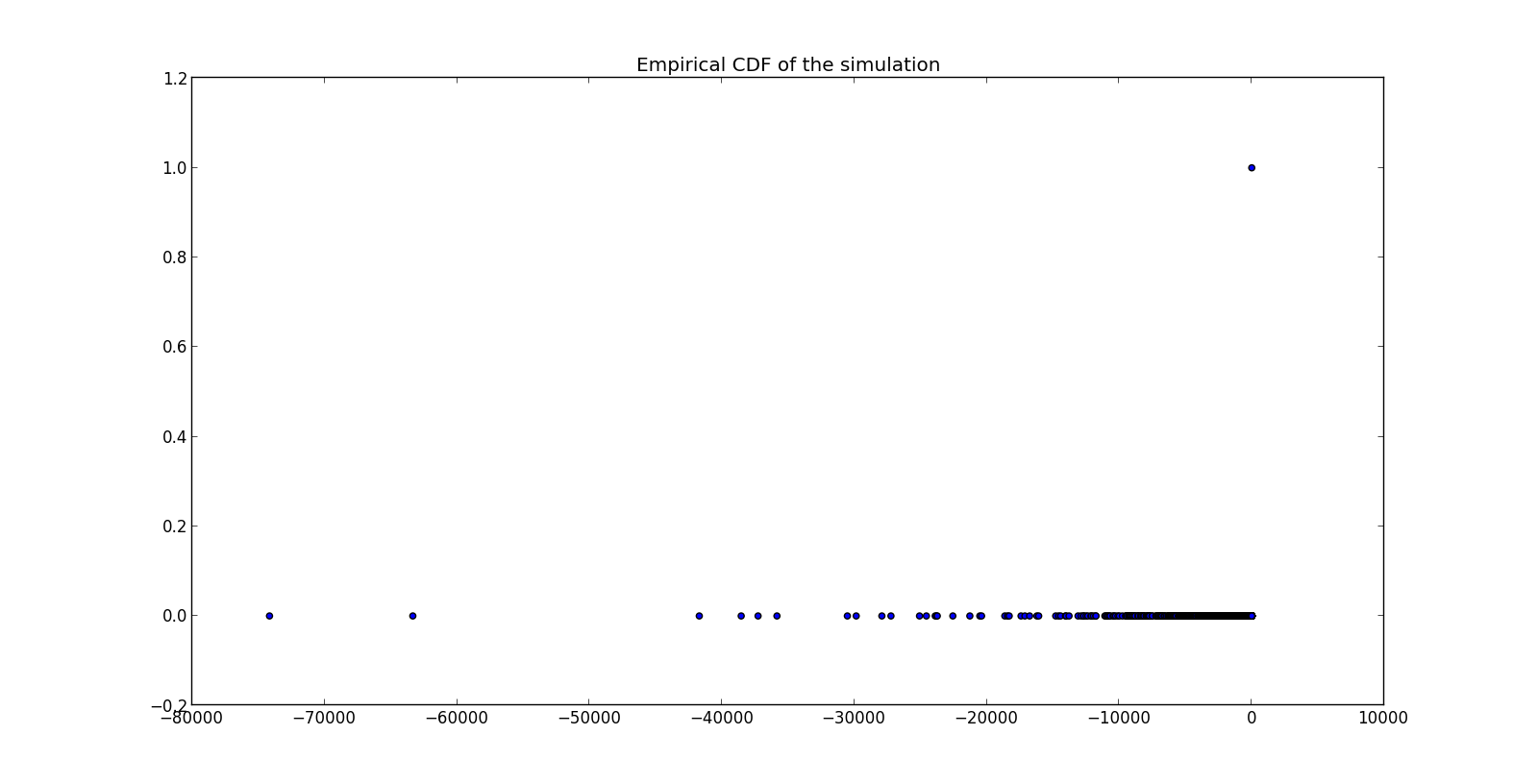

Judging from empirical CDF, this distribution is strange indeed. It simply looks like a value of 0 with 99.99% frequency, plus a smattering of large negative values. Is a lot of rounding involved?

With the highly skewed (non-symmetrical) distribution like this, the first thing I'd do is to take log(-X), where X are your sample values. If there are a lot of zeros, then you deal with censoring which is a rather complicated topic and you'll need to talk to a professional. A simple practical fix is just skip the zeros for now and work with strictly negative part of your sample.

EDIT: after looking at your original post, I notice that X is related to the stock price. IF this is a result of using some kind of geometric random walk (multiplying by some number at each step, for example), then it makes sense to do the entire simulation on the log scale (i.e. turn your multiplications into additions), then you will not get into the whole machine rounding situation and your X-values will be more meaningful.