I am trying fit an ARIMA model to stock returns.

I have reached a decent model using the AIC criterion.

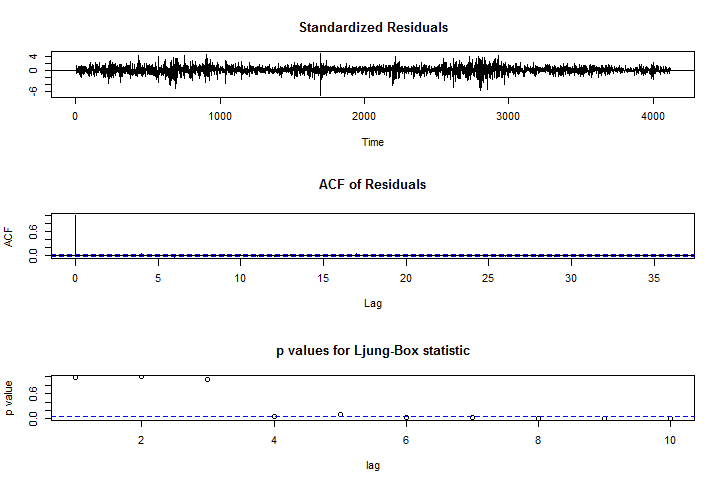

However, the ljung-box p value under a diagnostic plots are pretty weird. The null hypothesis get rejected at higher lags. I tried modifying the parameters, but L-B p value betters only marginally, with a loss in AIC.

Any help how I can balance the two ? Also any reasons why the p-value is so low for higher lags.

Ihave attached the diagnostic's image: