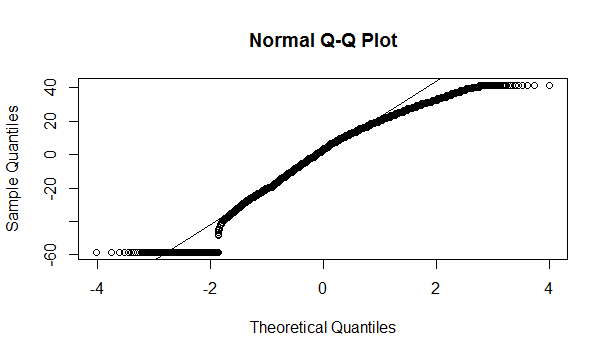

I am trying to model stock returns with the help of google trends data. As explained in my first question this data is normalised by google so that it is not normally distributed as User EdM kindly pointed out. Below I attached a qqnorm()plot for the accumulated values of some of my variables for further insight into their distribution.

Since my data is not normally distributed am I'm still allowed to do an OLS regression and look at performance measures like adjusted R squared and p-values? I saw some posts where it said that those tests are only used for normally distributed data, but that one can still use them due to the central limit theorem. Each variable has approximately 250 data entries in the in-sample data. Is this true? (Sorry, cannot find the posts atm and might be mixing something up)

Additionally, I would be really thankful if you could give me some further insights into model selection. I read a lot about it and as far as I understood it there are no set rules on how to find the best model and that it can get really complex the more variables you have. My problem is that I have more than 100 possible variables and - as far as my knowledge goes - those are simply too many. Hence, I thought I might be able to cut down on the variables by calculating the correlation (spearman) between every independent variable and the dependent variable. I would rank the correlations and start to cut out collinear variables (e.g. variabels that have higher absolute correlation than 0.5 with the variable I am inspecting). I know that I might lose some information by just watching correlation in the first place, but I dont know where else to start. I would do this until I get, lets say, 10 variables with relativ high correlation to the dependent variable and "low" collinearity. Then I would like to use stepwise or best subset regression to find the "best" model and finally use a rolling window approach or cross validation to approve the model.

As you might have guessed I am fairly new to regression statistics or statistics in general. I would be really thankful for any opinion or hint towards the right direction. I did a lot of research over the past few days, but couldnt simply find the right solution for the problems mentioned above.