I'm studying this time series (Italy - Producer Price Index):

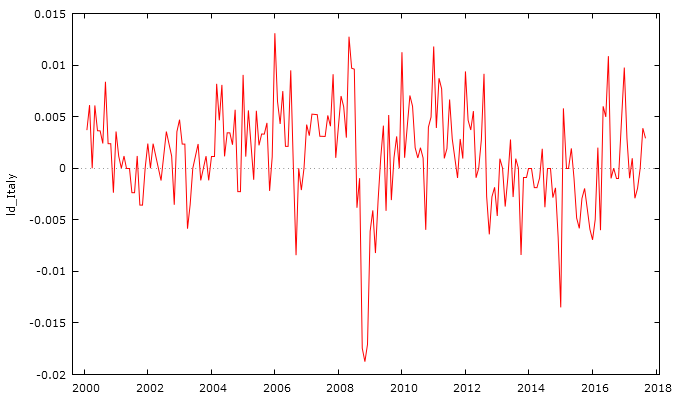

Using TRAMO for outlier detection, I have found an innovation outlier on October 2008. Differentiating the series, this outlier becomes a temporary change.

Using TRAMO for outlier detection, I have found an innovation outlier on October 2008. Differentiating the series, this outlier becomes a temporary change.

Is it possible this situation? Do you suggest to cut the series from the IO or to linearize the differentiated series?

Is it possible this situation? Do you suggest to cut the series from the IO or to linearize the differentiated series?

$\begingroup$

$\endgroup$

Add a comment

|

1 Answer

$\begingroup$

$\endgroup$

IO=TC When you have a stationary series and you correctly have differenced it

as a pulse =[1-B] STEP or a STEP=PULSE/[1-B]

or a pulse = [1-.99999]STEP if the transitional coefficient is approx 1.0

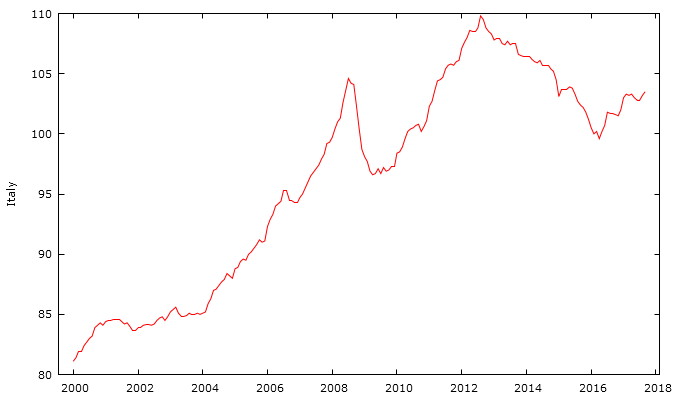

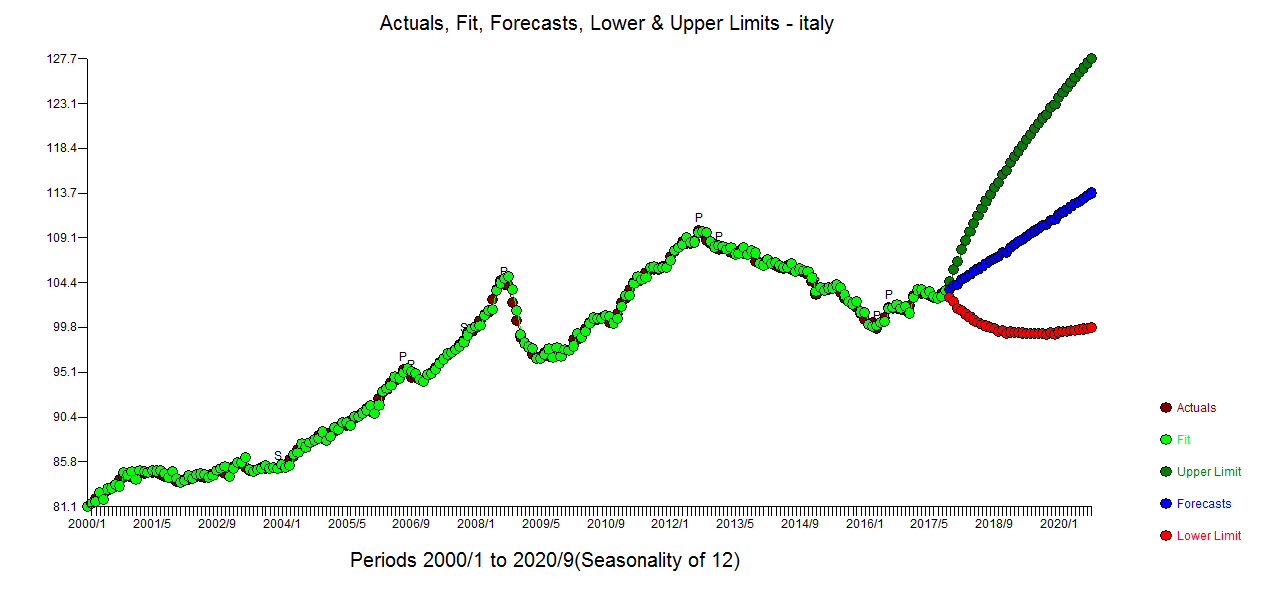

actual/fit and forecast for ITALY

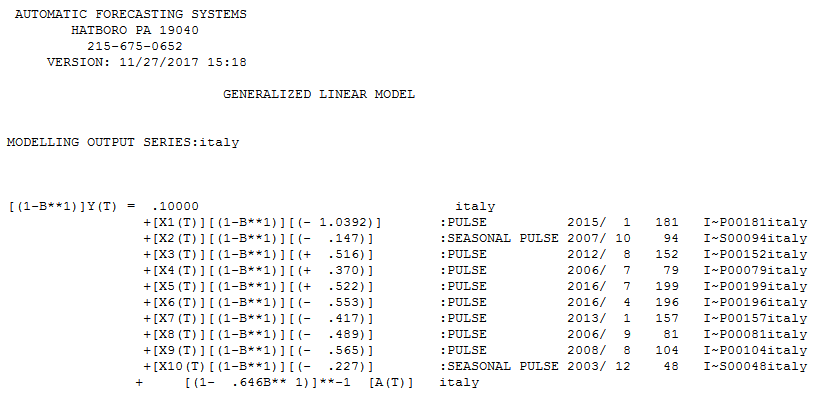

Equation suggesting 2 seasonal pulses with determinstic change in error variance (increased error variance at period 45)

Any attempt to seasonally difference this series will inject seasonality into the errors (slutzky effect) . Any software (or analyst) that suggests the need for seasonal differencing requires close inspection.