Apologies upfront! I know that similar questions have been asked before but I still can't wrap my head around it / I would like to have further clarification.

Let's have a look at the following time-series data:

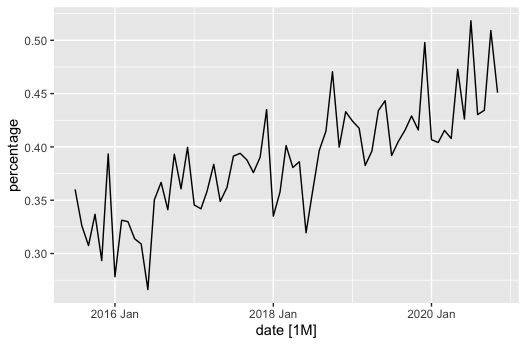

date percentage

<mth> <dbl>

1 2015 Jul 0.360

2 2015 Aug 0.326

3 2015 Sep 0.307

4 2015 Oct 0.337

5 2015 Nov 0.293

6 2015 Dec 0.393

7 2016 Jan 0.278

8 2016 Feb 0.331

9 2016 Mar 0.330

10 2016 Apr 0.314

# … with 55 more rows

percentage gives the share of how often a class of website got visited (0/1) i.e. in July 2015 the share of 1's visited was 36% in August 32.6% and so on ...

If you are plotting the complete data-set it looks something like this i.e. for the naive observer, a clear trend might be visible. My questions now are (with a focus on the first one):

(1) Did the percentage of class 1 websites significantly increase over time? (2) The percentage of class 1 websites viewed increased by at least X%

This is very similar to a question asked earlier: How to calculate the confidence that a trend in a time-series is positive?

However, the answer to this question hasn't been accepted and I don't know whether modelling the problem as a logistic regression would be reasonable in my case. Moreover, the second post in this question links to the following question: Determining trend significance in a time series

In this thread, one post suggested that using auto.arima() or more precisely regression with arima errors from the forecast package could be used to answer this question. However, I fail to see how this works/how the coefficient of such a regression can be interpreted whether it is a significant increase and by which % value. I also don't want to do forecasting. I just want to make a statement of whether there is a significant trend or whether this is random.

Moreover when trying this with my data using auto.arima() and its grid search would yield a completely different model than adding the time as regression parameters:

auto.arima(ts_test) vs. auto.arima(ts_test,xreg=t)

ts_test

ARIMA(0,1,1)(1,0,0)[12]

Coefficients:

ma1 sar1

-0.7871 0.3019

s.e. 0.0731 0.1541

sigma^2 estimated as 0.001219: log likelihood=123.88

AIC=-241.75 AICc=-241.35 BIC=-235.28

auto.arima with xreg

Series: ts_test

Regression with ARIMA(0,0,0) errors

Coefficients:

intercept xreg

0.3147 0.0022

s.e. 0.0079 0.0002

sigma^2 estimated as 0.001029: log likelihood=132.35

AIC=-258.7 AICc=-258.3 BIC=-252.17

So one can see that auto.arima uses quite a complex model with seasonal features, which the regression doesn't. Would this mean that I should do this manually? i.e. define the model like the first one and do the regression like this?

To be honest, I would rather try to avoid a complex approach like arima modelling, so could there not be an easier way to answer my initial questions (significant trend, what %) or if not how can I extract that from arima?

Looking forward to insights!