Despite their relative simplicity I've found it quite difficult to find a straightforward guide to copulas besides this short blog post. I went back through your code, fixed it up a bit and annotated what the steps were doing, but not why, as best I could if it should be of any use to others just starting out.

Update: After a bit more research I found this pdf, section 5 / pg 18 of which outlines pseudo code for a number of different copulas.

#a tcopula using rho = 0.8

#done from first principles

require(mvtnorm)

numObs <- 10000

#NX2 shaped matrix

initialObservations <- rmvnorm(numObs,mean=rep(0,2))

#this is a 2X2 symmetric matrix based off of rho=0.8 and is positive definite

psdRhoMatrix <- matrix(c(1,0.8,0.8,1),2,2)

#the transpose of the cholesky decomposition of the psdRhoMatrix

#which gives us a lower triangle matrix for some particular reason

lowerTriangleCholesky <- chol(psdRhoMatrix)

#this lower triangle matrix (for whatever reason) is able to make

#the observations in each column correlated

# NX2 = NX2 %*% 2X2

correlatedObservations <- initialObservations %*% lowerTriangleCholesky

degreesOfFreedom <- 2

#the meaning of this step eludes me, it's a vector of random chi-square observations.

#Maybe something to do with applying the inverse CDF.

randomChiSqrStep <- degreesOfFreedom/rchisq(numObs,degreesOfFreedom)

#transforming the correlated variables

#the random chiSquaredStep is applied to each column of the correlatedObservations

#for element wise multiplication to be properly applied the data needs to be

#sorted into columns rather than rows. NX2 = NX1 * NX2

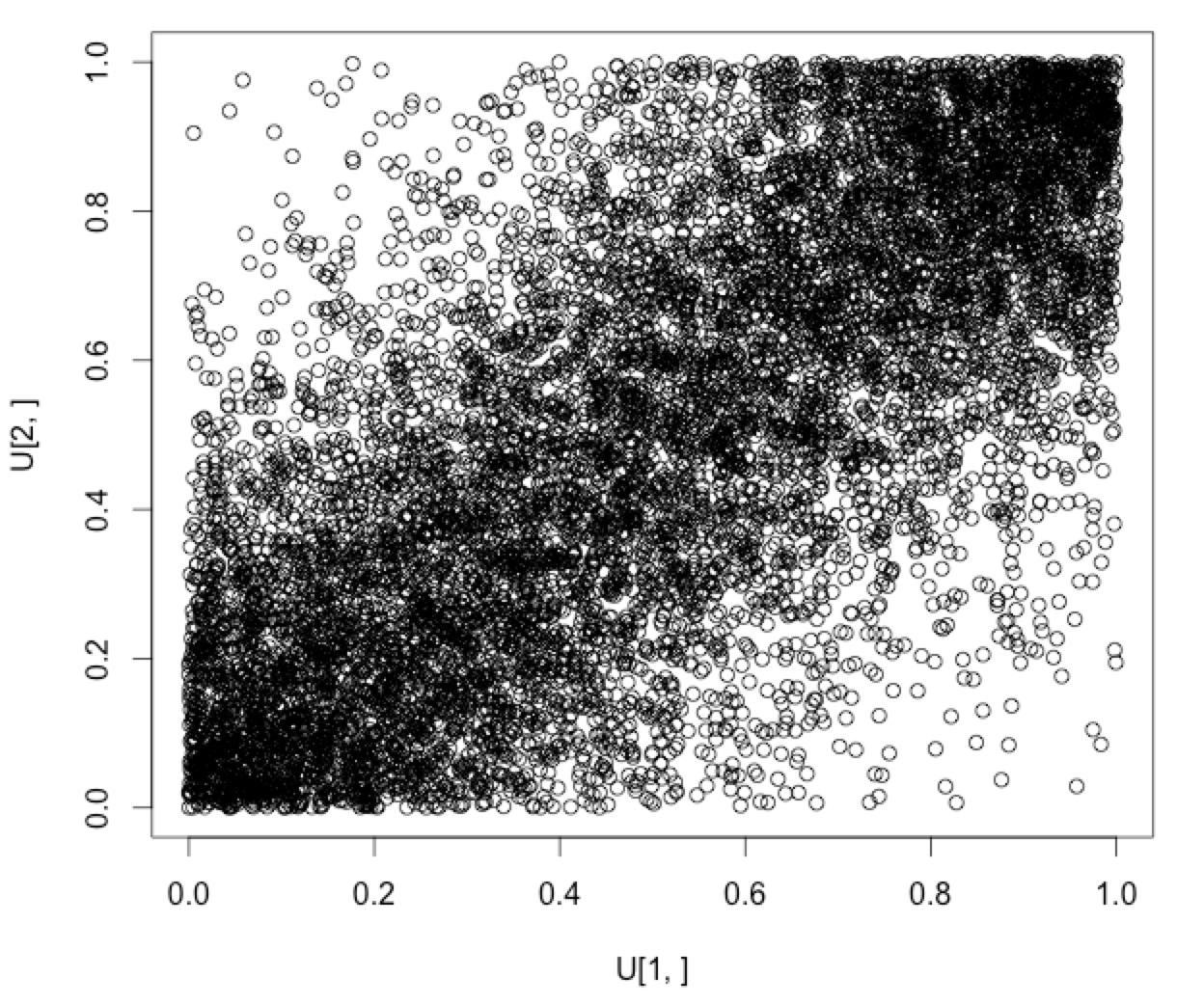

penultimateTransformation <- sqrt(randomChiSqrStep) * correlatedObservations

plot(penultimateTransformation[,1],penultimateTransformation[,2])

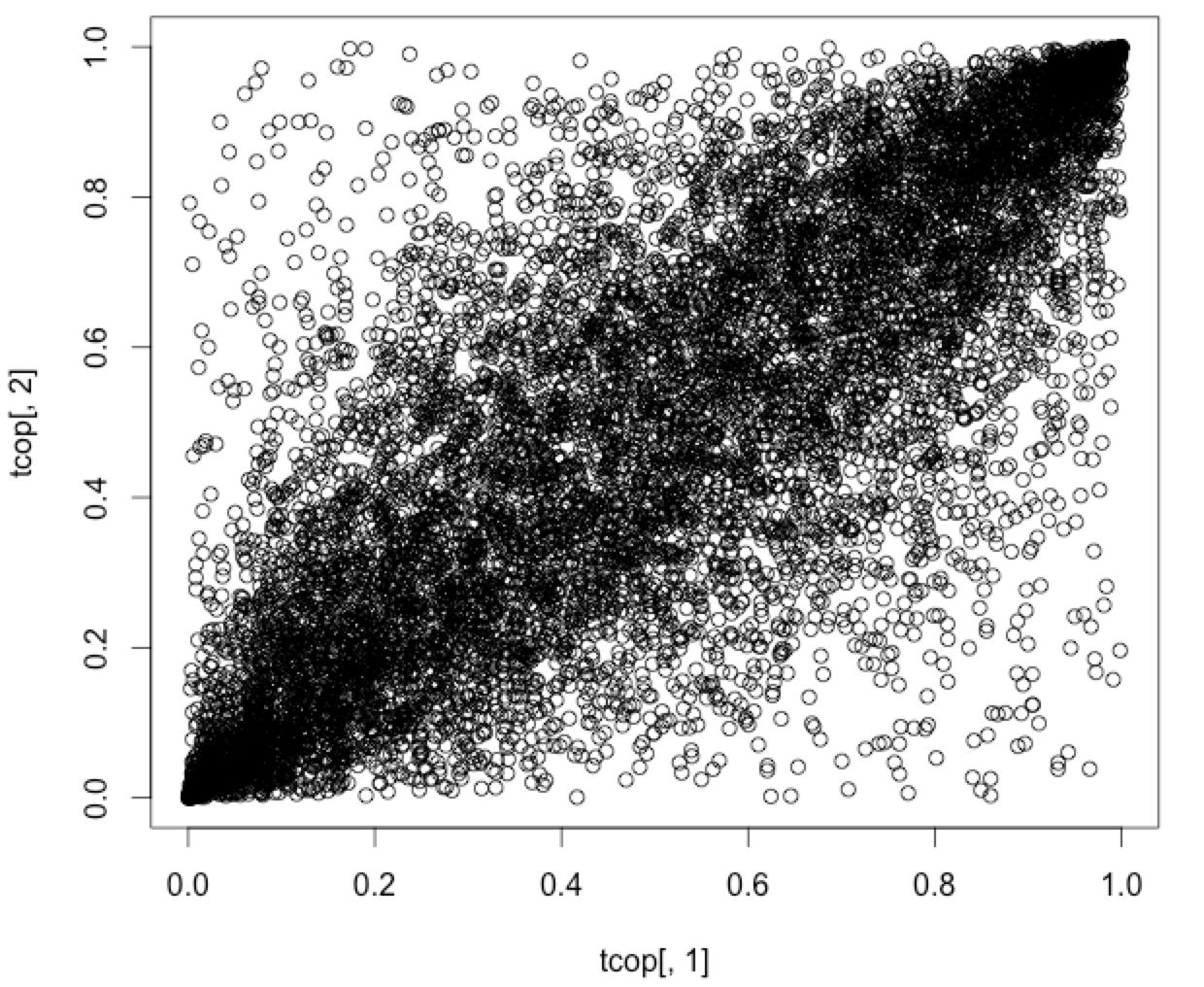

#run the fully transformed and correlated observations through the t-dist PDF and that's it

tCopulaOutPut <- pt(penultimateTransformation,degreesOfFreedom)

plot(tcopulaOutPut[,1],tcopulaOutPut[,2])

Does anyone know if I'm making a conceptual error or a mistake in the code?

Does anyone know if I'm making a conceptual error or a mistake in the code?