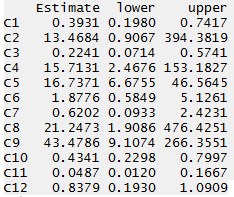

I have estimated a binary logit and calculated the odds ratios and their LR confidence intervals as follows:

As you see some of these intervals are extremely wide. I guess it is due to insufficient variability in those variables (but I am not sure). How should I interpret these in a research paper? Should I just say (e.g. for C8) "c unit increase in x changes the odds of success by 1.9086 to 476.4251 times, with 95% confidence"? I am sure the reviewers will find this and point at it. What is your suggestion?