A problem is that you're running multiple (at least two) tests here, and the more tests you run, the more likely is it to have a meaningless rejection of a null hypothesis. So in the first place I'd be interested in the precise p-value of the second test, and if this is just below 0.05, I wouldn't interpret this as clear evidence against independence.

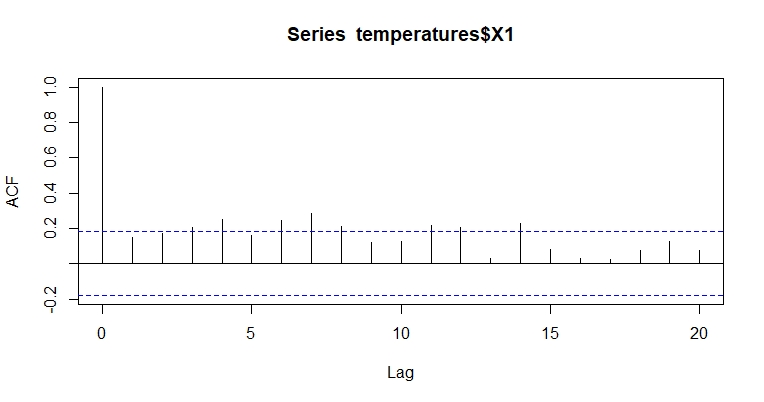

Anyway your plot suggests that there might be weak long range dependence (or let's say moderately long range). There isn't any "contradiction" in your results as it may well be that you need to look at lags larger than one to find this. To what extent this will affect your further analysis I can't tell. It may not be that much of a problem, but then this depends on what exactly you want to do.

Note that there is a general misunderstanding about model assumptions. Models are by their very nature idealisations, and model assumptions will never hold precisely. What is important is whether models are violated in ways that mislead the later analysis you want to run. Unfortunately running model misspecification tests as you do here isn't always reliable for addressing this issue. Also note that not rejecting a model assumption does not mean it's true. Particularly Ljung-Box itself could be affected by outliers, so you should look at your actual data to see whether there might be a problem there.