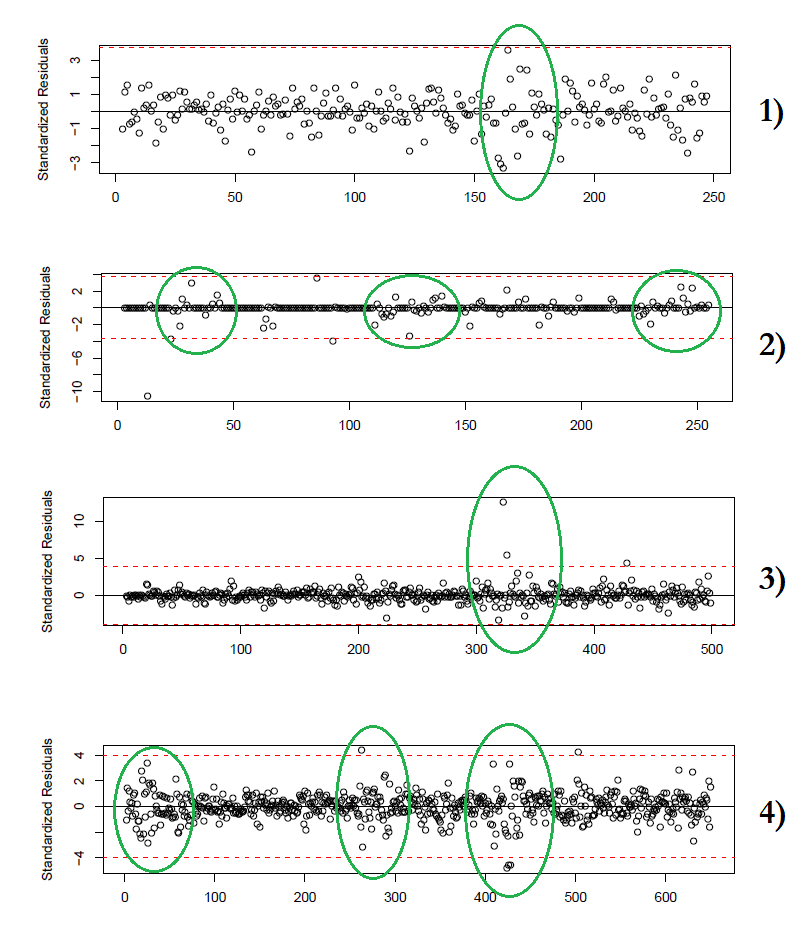

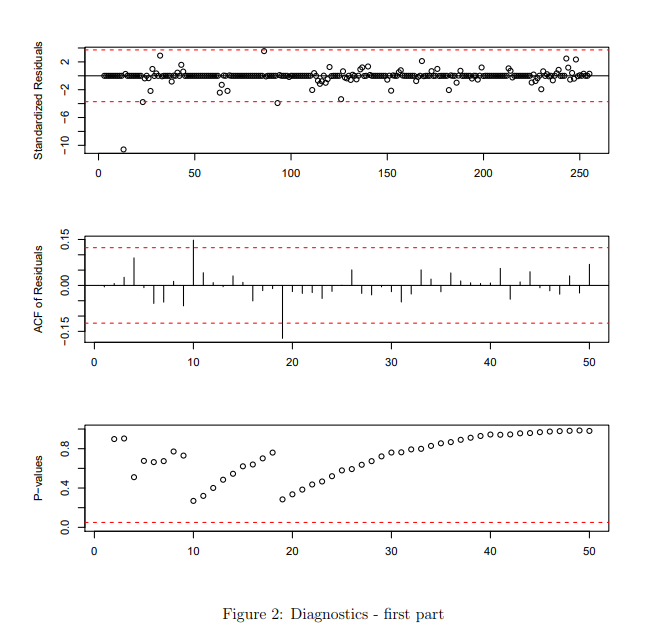

I'm practising in the individuation of heteroskedasticity from the standardized residuals.

I know that, if the time series is homoskedastic, the spread of the residuals should be constant and random around zero-mean.

About my problem, I'm having trouble in the interpretation of the followings plots. I evidenced (with the colour green) the significant parts that, in my opinion, could suggest me that the time series has heteroskedasticity.

The parts that I pointed out, are significant or they are just anomalies? Any help would be appreciated

Edit

I add the text from the exercise where I found the standardized residuals of graph 2.

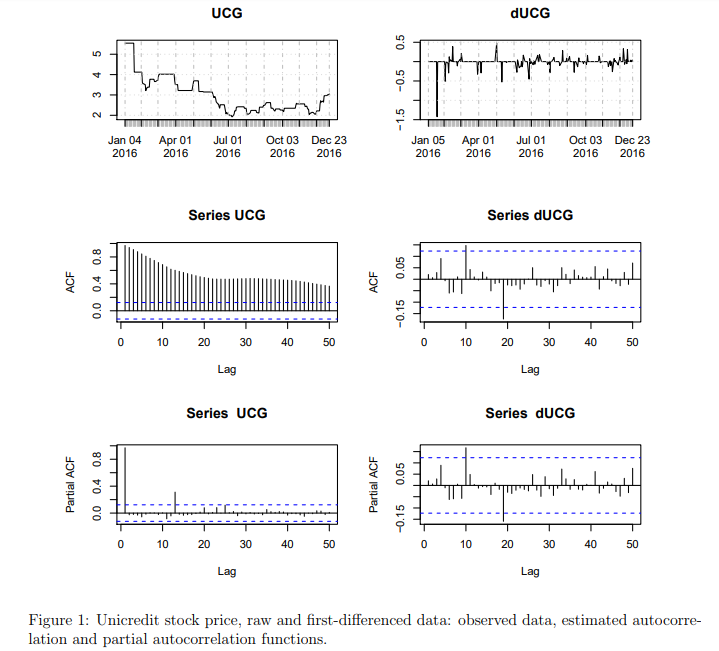

The time series of interest is the Unicredit stock price index at Milan stock market, from 2015-01-02 to 2016-12-23. Figure 1 shows the raw (UCG) and first differenced (dUCG) data together with the estimated autocorrelation and partial autocorrelation functions. The following ARIMA(0, 1, 1) model has been fitted:

Call:

arima(x = UCG, order = c(0, 1, 1))

Coefficients:

ma1

0.0253

s.e. 0.0620

sigma^2 estimated as 0.01808: log likelihood = 149.24, aic = -296.47

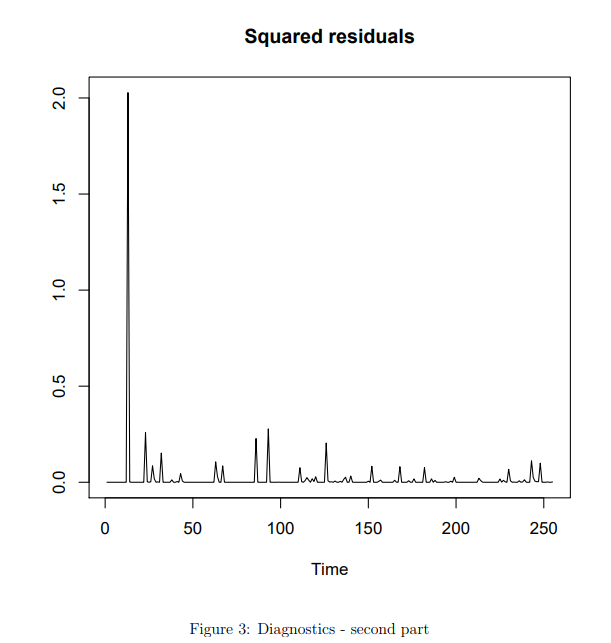

The diagnostics on the residuals are shown in Figure 2 and 3

As you can see the exercise doesn't give me a QQnormal plot in order to identify the distribution of my residuals (in this case the residuals of graph 2, first picture).

Is there another way to confirm if the standardized residuals show homoskedasticity or not?