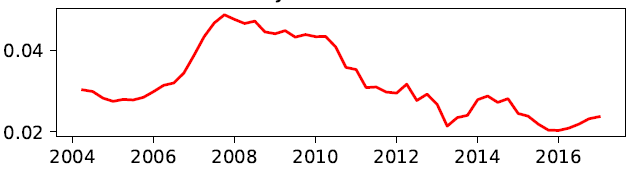

I attached the graph of a time series below, which is a series of the probability of defaults. This is a quarterly time series. When I am using a regression model to forecast this time series, should I test the structural breaks? And if so, should I only use the coefficient of the most recent time window to forecast the time series?

This is a quarterly time series. When I am using a regression model to forecast this time series, should I test the structural breaks? And if so, should I only use the coefficient of the most recent time window to forecast the time series?

But what if this is just a cycle or part of a cycle, that in the next few years, the trend is going up again. In this sense, should I keep using the coefficients after the break, or should I ignore the structural break?

The regression model I am using would be

$PD_t=\alpha+\beta Macro\ variable_t+\epsilon_t$