Using Stats models and Pandas (and requests for the data) I'm working on a forecast model.. my 1st step is just getting the Arma function working and understood. My data is available publically and is highly seasonal residential real estate unit sales data, I'm planning to see how a quarterly survey that we do can help with the forecast as a later step. Hence why I am changing the frequency to quarterly with dates that match the dates I have on the quarterly survey.

So the code looks like:

#get the statewide actual data from Sheet 1 parse dates and select just unit sales

act = requests.get('https://docs.google.com/spreadsheet/ccc?key=0Ak_wF7ZGeMmHdFZtQjI1a1hhUWR2UExCa2E4MFhiWWc&output=csv&gid=1')

dataact = act.content

actdf = pd.read_csv(StringIO(dataact),index_col=0,parse_dates=['date'], thousands=',') #converts to numbers

actdf.rename(columns={'Unit Sales': 'Units'}, inplace=True)

actdf=actdf[['Units']]

actdfq=actdf.resample('Q',sum)

actdfq.index = actdfq.index + pd.DateOffset(days=15) #align the actual data dates to the survey dates Eg the 15th of the quarter

actdfq=actdfq['2009':] # selcts the time periods for which we have surveys (actual results here) The survey would be shifted back by one

actdfqchg=actdfq['Units']

fig = plt.figure(figsize=(12,8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(actdfqchg.values.squeeze(), lags=4, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(actdfqchg, lags=4, ax=ax2)

the data looks like:

2009-01-15 7867

2009-04-15 7483

2009-07-15 10109

2009-10-15 10648

2010-01-15 9678

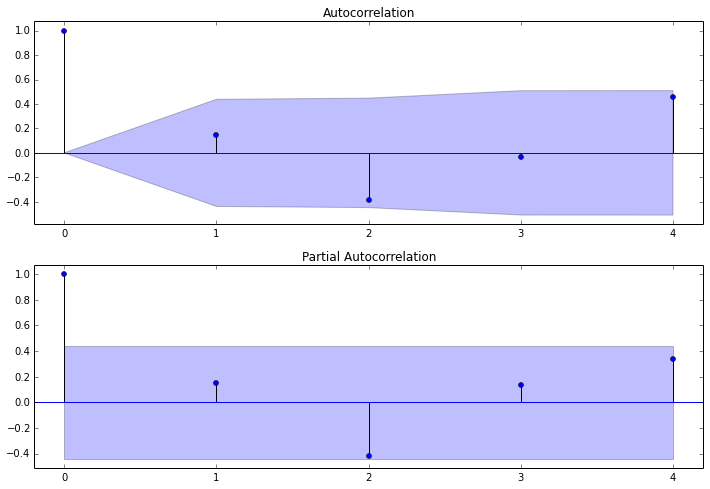

The acf graphs look like:

So I don't really know what the ACF is telling me..The graph of auto correlation would tend to tell me that the 4q correlation is the strongest but still only .4? (correct?) and the 2q score of -.4 would indicate that the summer to winter correlation would be the weakest (which makes sense) and how to proceed with 1) a projection based on this actual data just using straight Arma Stats models capabilities.

and 2) how to best incorporate survey data that attempt to predict the following quarter.. the survey is taken asking for predictions for the following quarter on a 5 point scale with a400+ participants, the straight correlation is not super strong but I think somehow I should be able to find the quarterly correlation to help inform the projection for the subsequent quarter..??