You can just use the fact that the correlation at any time $t$ of two series in the DCC GARCH

model, $Y_{1t}, Y_{2t}$ is just $\tfrac{\mathbb{C}(Y_{1t}, Y_{2t})}{\sqrt{\mathbb{V}(Y_{1t})\mathbb{V}(Y_{1t})}}$.

You can compute this manually as in the following example

webuse stocks, clear

// fit the DCC GARCH model

mgarch dcc (toyota nissan = , noconstant) (honda = , noconstant), ///

arch(1) garch(1)

// predict the conditional covariances

predict condvar*, variance

// generate the correlations

g condcorr_nissan_toyota = condvar_nissan_toyota/ ///

(sqrt(condvar_nissan_nissan)*sqrt(condvar_toyota_toyota))

g condcorr_honda_toyota = condvar_honda_toyota/ ///

(sqrt(condvar_honda_honda)*sqrt(condvar_toyota_toyota))

g condcorr_honda_nissan = condvar_honda_nissan/ ///

(sqrt(condvar_nissan_nissan)*sqrt(condvar_honda_honda))

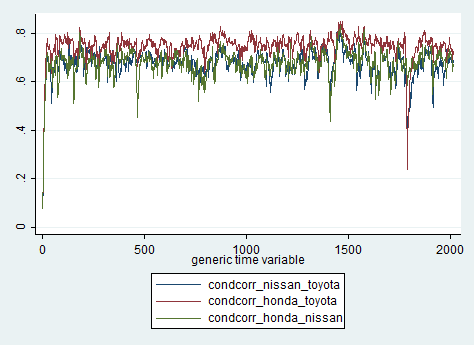

// plot the conditional correlations

tsline condcorr_nissan_toyota condcorr_honda_toyota condcorr_honda_nissan, ///

legend(rows(3))