I am analyzing this data.

Here is my code

library(fpp)

library(urca)

setwd("C:/Users/kuco/Desktop") #where is the file folder

dt<-read.csv("test.csv",header = FALSE) #read the file

t<-ts(dt,start = c(1997,1),frequency = 12) #put it into time series data

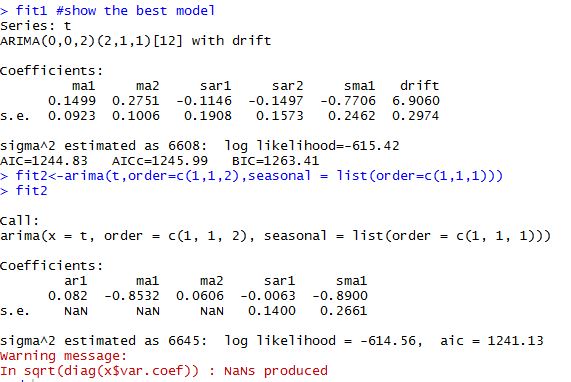

fit1<-auto.arima(t,stepwise = F,approximation = FALSE,ic="aic",D=1) #find the best model

fit1 #show the best model

fit2<-arima(t,order=c(1,1,2),seasonal = list(order=c(1,1,1)))

fit2

But it turns out that the arima(1,1,2)(1,1,12)[12] is better than the model from auto.arima(). So what can I do to get the lowest AIC model?

auto.arima, you will see that AIC is used within a fixed order of integration, but not across them. The order of integration (seasonal and simple) is determined by tests (OCSB and KPSS, respectively). $\endgroup$