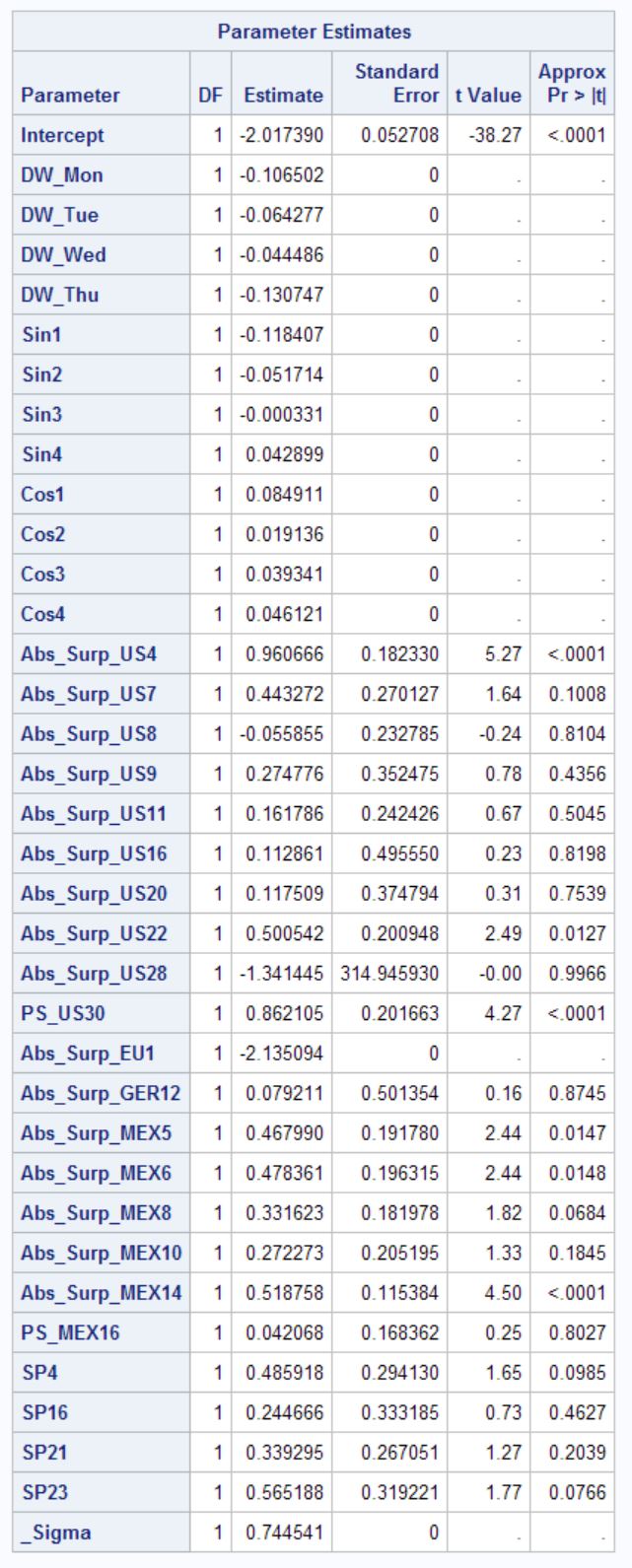

This typically happens when your Hessian matrix is nearly singular. The following SAS article describes your exact situation I believe.

http://support.sas.com/kb/31/714.html

Try re-scaling the variables that have zero standard errors as this is most likely the cause of the problem you are experiencing. I'm guessing that these variables are measured on a scale that is significantly larger/smaller than your other variables, which is leading to the invertibility problems with the Hessian matrix.

You're likely to resolve this problem by standardizing the predictors before running proc qlim. See proc standard for this. Verify that you have correctly specified your model and didn't accidentally include some variables twice. It seems this has lead to some other problems noted here (the answer there by @placidia is a good one and may help you resolve your issue with proc qlim).

If that does't work, try reading through this article and try some of the suggestions there.