I would like to ask you, how to correctly interpret different results for different number of lags in arch.test (R)? We reject the null hypothesis (homoscedasticity) up to 12th lag but after that we fail to do so. So, what does it mean that our time series looks homoscedastic (no ARCH effects) for lags=4 and 8, but for lags=12 and above result is heteroscedastic?

$\begingroup$

$\endgroup$

1

-

$\begingroup$ Your 2nd and 3rd sentences seem to be contradictory. $H_0$ is homoskedasticity, i.e. absence of ARCH effects. If you reject $H_0$, then you reject absence of ARCH effects, i.e. they seem to be present. $\endgroup$– Richard HardyCommented Jun 4, 2023 at 12:43

Add a comment

|

1 Answer

$\begingroup$

$\endgroup$

$\endgroup$

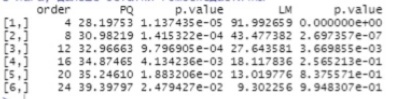

This is a common weakness of portmanteau-type tests. When we think there may be nonzero autocorrelation at some lag(s) but we do not know which one(s), we can inspect multiple lags at once. This is what the ARCH-LM test does. If there is nonzero autocorrelation at only one* lag among a few that we are inspecting, this may be enough to reject $H_0$. If it is one among many, this may not move the needle enough to reject $H_0$. This is also what you see.

The tricky thing is what to conclude from the results you got. I think it is pretty clear that there is strong autocorrelation at low-order lags, and that calls for a GARCH model. (Note that $H_0$ is homoskedasticity and $H_1$ is heteroskedasticity of ARCH type, and a low $p$-value points to rejecting $H_0$.) There is zero or low autocorrelation among high-order lags, but that just suggests the autoregressive component of GARCH (the $\beta$ coefficient in GARCH(1,1)) is not that strong while the moving average components (the $\alpha$ coefficient in GARCH(s,1)) is.

*It could be a few, but still a small number.

answered Jun 4, 2023 at 12:39